Tracking what you pay to invest is one of the highest‑impact money habits you can build in 2025. Fees look tiny on paper—0.5% here, 1% there—but quietly eat into decades of compounding. This guide walks you through a practical, repeatable way to see what you’re paying, decide whether it’s fair, and cut the fat without blowing up your strategy.

—

Why your investment fees quietly matter more than you think

A one‑time 1% charge feels like pocket change. But an extra 1% fee every year, for 30 years, can wipe out tens or even hundreds of thousands of dollars from a retirement portfolio. That’s because fees reduce your returns *every single year*, and future gains are earned on a smaller base.

You don’t need to become a finance pro. You just need a systematic way to spot where fees hide, measure them in dollars, and make smart trade‑offs. Think “basic health check,” not “open‑heart surgery.”

—

Essential tools to track and assess your investment fees

1. Account statements and fee disclosures

Start with the basics: grab your latest brokerage, retirement, and robo‑advisor statements. Download the PDFs if you can. Then find each account’s “fee schedule” or “relationship summary” on the provider’s website—these documents usually show advisory fees, commissions, and common transaction costs.

You’ll also want the summary prospectus or factsheet for each fund or ETF you own. That’s where the ongoing expense ratio and other embedded costs live.

—

2. A simple spreadsheet (or note‑taking app)

You don’t need fancy software. A spreadsheet with a few columns—Account, Investment name, Ticker, Value, Expense ratio, Advisory fee, Other fees—is more than enough. If spreadsheets scare you, a notes app works too, as long as you list each investment and its fees in some consistent way.

Short version: if you can add and multiply, you can do this.

—

3. A trusted investment fee calculator

Online tools make it easier to turn abstract percentages into concrete dollars. An investment fee calculator lets you plug in your portfolio value, estimated annual return, and various fee levels to see how much each scenario costs over 10, 20, or 30 years. You’re not aiming for perfection—just a clear sense of scale: “Is this fee likely to cost me hundreds…or six figures?”

—

4. Independent research sources

To cross‑check fees and compare your options, you’ll want at least one independent source: a fund rating site, your country’s financial regulator pages, or well‑known investing publications. These help you sanity‑check whether your funds are “cheap,” “average,” or “expensive” for their type.

—

Step‑by‑step: how to track and assess your investment fees

Step 1: List every account and where it lives

Create one list of all your investing accounts:

1. Employer plans (401(k), 403(b), etc.)

2. IRAs or other tax‑advantaged accounts

3. Taxable brokerage accounts

4. Robo‑advisors and managed portfolios

5. Legacy or “forgotten” accounts (old workplace plans, annuities, etc.)

Next to each one, note the provider name (for example, Vanguard, Fidelity, your bank, or a robo‑advisor) and the current balance. This sounds boring, but it prevents you from missing fees in an old, dusty account you haven’t touched in years.

—

Step 2: Capture what you pay at the account level

Many fees are charged on the whole account, not on individual funds. Look for:

– Advisory or management fee (often 0.25–1.5% per year)

– Platform or “custody” fee (sometimes a flat annual amount)

– Wrap fees for “managed accounts”

If your advisor or platform takes 1% of total assets each year, write that down clearly. This is often the single biggest line item.

This is where you’re essentially getting “investment management fees explained” for your own situation: ongoing advice, portfolio monitoring, asset allocation, and maybe planning services bundled into one number.

—

Step 3: Record fees for each fund, ETF, and product

Now drill down into what you actually own:

– For mutual funds and ETFs, find the *expense ratio* (e.g., 0.08%, 0.65%, 1.20%).

– For active funds, also look for performance fees or loads (front‑end or back‑end sales charges).

– For structured products or complex notes, identify any embedded product fees.

Enter each holding into your spreadsheet with:

– Name and ticker

– Current value

– Expense ratio

You’ve just built your personal fee map.

—

Step 4: Turn percentages into actual dollars

Percentages hide emotional impact. Convert them into annual dollar costs:

– Annual fund cost ≈ Account value in that fund × Expense ratio

– Annual advisory cost ≈ Account balance × Advisory fee

Do this for each major holding and each account. Add them up to get your total annual fee in dollars.

A rough example:

– $100,000 in a 0.80% fund ≈ $800 per year

– $100,000 under a 1.00% advisor fee ≈ $1,000 per year

Together that’s $1,800 per year—or $18,000 over ten years before even considering compounding.

—

Step 5: Learn how to compare investment fees fairly

Now that you know what you’re paying, the next question is how to compare investment fees in a way that’s actually useful.

You want apples‑to‑apples comparisons:

– Compare index funds to other index funds tracking the same or similar index.

– Compare active funds to other active funds in the same asset class and region.

– Compare robo‑advisors and human advisors by looking at *all‑in* cost (underlying fund fees plus platform or advisory fee).

If a fund charges 0.75% and you can find a nearly identical index fund at 0.05%, the expensive one needs to justify its cost with a very strong and persistent track record, not just a good year or two.

—

Step 6: Judge whether each fee is “worth it”

Not all fees are bad. The key is alignment: are you paying for something you actually value and use?

Consider:

– Complexity: If your situation is simple (single person, long horizon, basic goals), you may not need high‑touch management.

– Behavioral support: If an advisor keeps you from panicking in downturns, that can easily be worth their fee.

– Access to strategies: Institutional‑class funds or specialized planning may justify higher costs.

When a fee doesn’t clearly buy you something you care about—simplicity, better service, or meaningful odds of better risk‑adjusted returns—it becomes a candidate for trimming.

—

Cutting unnecessary costs without breaking your plan

Prioritize the big wins first

You’ll usually see the biggest savings from:

– Lowering advisory or platform fees if they’re high

– Swapping expensive funds for cheaper equivalents

– Moving away from complex, high‑fee products that you don’t really need

Don’t obsess over a 0.01% difference. Focus on the 0.5–1.5% chunks.

—

How to reduce mutual fund and ETF fees intelligently

A practical way to reduce mutual fund and ETF fees is to:

– Replace high‑cost active funds that simply mirror the market with low‑cost index funds.

– Consolidate very similar funds to avoid paying multiple layers of fees for overlapping exposure.

– Use institutional or “premium” share classes if your account size qualifies.

Always check for tax consequences before selling in taxable accounts. In retirement accounts, switching is usually tax‑free, so it’s easier to optimize there first.

—

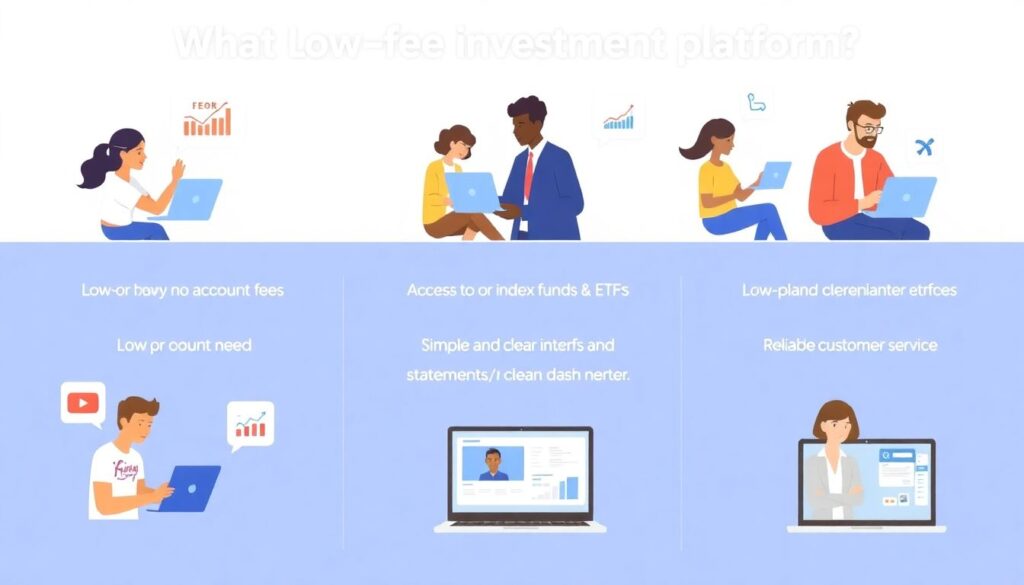

Choosing the best low fee investment platforms for you

The best low fee investment platforms for one person might not fit another. You’re looking for a good balance of:

– Low or no account fees

– Access to cheap index funds and ETFs

– Simple, clear interfaces and statements

– Reliable customer service

If you like guidance but want to keep costs lean, a low‑cost robo‑advisor plus low‑fee index funds is often cheaper than a traditional 1% advisory model. If you’re comfortable managing your own allocation, a no‑frills brokerage that charges close to zero in commissions and account fees can keep ongoing costs minimal.

—

Troubleshooting common problems when tracking fees

Problem 1: You can’t find the fees

Sometimes providers bury fee details in dense documents. If you’re stuck:

– Search for terms like “expense ratio,” “fee schedule,” or “Form CRS” on the provider’s site.

– Call customer support and ask: “What is my total advisory fee, and what are the expense ratios of my current holdings?”

– For employer plans, check the annual “fee disclosure” notice you get (often ignored and deleted—go recover it).

If a provider is vague or evasive, treat that as a red flag.

—

Problem 2: Jargon overload

You might see multiple terms—advisory fee, wrap fee, 12b‑1 fee, loads—and feel lost. When that happens, simplify:

– Separate fees into two buckets: ongoing percentage fees (taken each year) and one‑time fees (commissions, loads, transaction charges).

– Focus first on ongoing percentage fees; these are usually the biggest long‑term drag.

If you can answer “What percentage of my assets do I lose each year in total fees?” you’ve cleared the most important hurdle.

—

Problem 3: Fear of making a change

It’s normal to worry you’ll mess things up if you switch investments. To manage that:

– Change only one account at a time.

– Keep your overall risk level and asset mix similar when swapping funds.

– If you’re unsure, ask a fee‑only planner—someone who charges a flat or hourly rate and doesn’t earn commissions on products.

Remember: doing *nothing* also has a cost if your fee burden is high.

—

Building an ongoing fee checkup routine

Set a calendar reminder

Fees are not a one‑time project. Providers change pricing, new cheaper funds launch, and your balance grows, making the dollar impact of the same percentage fee larger.

A simple system:

– Once a year, review your total fees per account and per fund.

– Every 3–5 years, reevaluate whether you still need the same level of advice or complexity.

This turns fee management from a stressful overhaul into a predictable habit.

—

Track your progress in real money terms

Each time you lower a fee, note how much you’re saving annually:

– “Switched bond fund: saved $120 per year.”

– “Cut advisory fee from 1% to 0.4%: saved $1,200 per year.”

Then run those numbers through your investment fee calculator again to see the 20‑ or 30‑year impact. Seeing “I just freed up $50,000–$100,000 of future wealth” is strong motivation to keep going.

—

What’s next: the future of tracking and managing investment fees (2025 and beyond)

Automation, transparency, and regulation are all moving in your favor

As of 2025, three big trends are reshaping how we deal with fees:

1. Better data and aggregation tools

More apps and platforms are pulling in all your accounts, reading fee data directly from statements, and summarizing your “total cost of ownership” automatically. Expect more one‑click dashboards showing, in plain English, how much you paid in fees this year and where.

2. AI‑driven recommendations

Tools are already emerging that scan your portfolio, flag high‑fee investments, and suggest lower‑cost alternatives that match your risk profile. Over the next few years, expect consumer‑grade “fee coaches” that can simulate different choices and highlight the trade‑offs in seconds.

3. Regulatory pressure for clarity

Regulators in many countries are pushing for investment management fees explained in simpler, standardized language. We’re likely to see more mandatory dollar‑amount disclosures (“You paid $X in fees this year”), clearer visual breakdowns, and tougher rules around hidden or layered costs.

—

What this means for everyday investors

Over the rest of the 2020s:

– The fee gap between high‑cost and mainstream options should continue to shrink, especially in broad index investing.

– Personalized portfolios delivered at robo‑level prices will become common, narrowing the advantage of traditional high‑fee advisory models.

– Investors who *do* pay more—whether for a niche strategy or specialized planning—will increasingly demand proof of value, not just nice branding.

Those who build the habit of tracking and questioning fees now will be in the best position to harness these changes. Instead of guessing whether you’re overpaying, you’ll have hard numbers, better tools, and more competitive options.

—

Bringing it all together

You don’t need to memorize every term in the fee dictionary. You just need a repeatable process:

– Gather statements and disclosures.

– Map your accounts and holdings.

– Convert percentage fees into real dollars.

– Compare your costs to reasonable alternatives.

– Trim what you don’t need, keep what truly adds value, and recheck once a year.

That’s how you turn opaque, confusing charges into something you can see, measure, and control—and let more of your money do what it’s supposed to do: grow for your future.