Why your money keeps “disappearing” each month

You’re not bad with money; you’re just flying without instruments. Most people who say “I have no idea where my salary goes” aren’t wasting it all on luxuries. It’s coffee runs, quick deliveries, subscriptions, and mini-impulse buys that slowly eat the budget. A 2023 survey by Intuit found that the average person underestimates their monthly card spending by 20–25%. So if you think you spend $1,000, odds are it’s closer to $1,200–$1,250. That gap is the “leak” in your monthly budget, and until вы начнёте реально отслеживать расходы, любые попытки экономить будут напоминать черпание воды из лодки без закрытой пробки. Не нужно превращаться в бухгалтера 80-го уровня — достаточно пары простых привычек и правильных инструментов.

Most people don’t need a complicated financial system; they need a clear picture of where money goes in the next 30 days.

Expert view: tracking before cutting

Financial planners repeat one thing like a mantra: don’t start with strict limits, start with observation. CFPs (Certified Financial Planners) often recommend tracking every expense for at least 30 days before changing anything. Only after that month do you see that your “occasional” taxi rides cost $90, food delivery another $120, and three “small” subscriptions total $45. That’s already $255 you can optimize without touching rent or groceries.

Method 1: The 10‑minute daily money check-in

If you hate spreadsheets and apps, this method is your entry point. Every evening, spend 10 minutes writing down what you spent that day. Pen and notebook, or a simple note on your phone – doesn’t matter. The point is to connect the action (“I tapped the card for $18”) with the number. After a week, patterns jump out: “Why did I buy food twice in one day?”, “Did I really need that extra subscription?” Psychologists call this “bringing behavior into awareness”, and it works better than vague resolutions like “I’ll spend less this month”. You’re not judging yourself, you’re just gathering data like an investigator.

Here’s the twist: for many people, this small ritual quickly becomes more effective than even the best expense tracking apps, because it builds a habit of conscious spending, not just background recording.

Technical block: what exactly to write down

– Date and total income for the month (once, on payday)

– Every expense over $1 with category: “Lunch – $9”, “Taxi – $13”, “Streaming – $5”

– Big fixed costs first: rent, utilities, loan payments

– At the end of each week, total by category: food, transport, fun, “junk”

If you have 20–30 lines a day, that’s normal. If you have 60+ micro-payments, it’s a sign that your money leaks live in small, frequent purchases.

Method 2: Simple 50/30/20 plan that actually survives real life

The classic rule says: 50% of your income goes to needs, 30% to wants, 20% to savings and debt payments. In practice, in big cities housing alone can eat 40–45%. So experts now use this as a direction, not a law. Look at your last three months and calculate rough percentages. If your “wants” category (cafes, subscriptions, impulse shopping) is over 35–40%, you’ve found a major leak. Most clients I’ve seen manage to free up $100–$300 a month just by trimming this area down by a few percent and redirecting the freed money to savings.

Short version: don’t chase the perfect formula; use the 50/30/20 structure as a map to see which part of your budget is bloated.

Expert tweak: the 1% monthly upgrade

Instead of painfully jumping from 0% savings to 20% at once, increase your savings rate by 1% of income every month. Earn $2,000? That’s just $20 more this month. In a year you’ll go from 0% to 12% almost безболезненно, and you’ll barely notice the small monthly adjustments.

Method 3: Using apps and software without drowning in features

Digital tools can automate half of the work. The trick is not to chase the best expense tracking apps by rating, but to choose one that matches your personality. If you rarely open apps, set up one that works mostly in the background and syncs with your bank. If you like control, choose something where you manually tag each expense and see pretty charts. Many people drop fancy monthly budget tracking software because it asks them to categorize each transaction into 25 subcategories. Nobody does that longer than two weeks. Keep it to 5–7 broad categories: housing, transport, groceries, eating out, fun, subscriptions, “other”.

Think of it like a fitness tracker: it doesn’t make you fit, but it shows patterns. Seeing that you spent $310 on food delivery last month sometimes hits harder than any lecture about “financial discipline”.

Technical block: how to set up an app in 15 minutes

– Turn on automatic import of bank and card transactions

– Disable exotic categories, leave only 5–7 main ones

– Set weekly notifications: “Here’s your spending vs last week”, not just “You hit your limit”

– Add your fixed monthly bills as recurring: rent, internet, phone, loans

– Set one savings goal, not five: e.g. “Emergency fund $1,000”

Most modern personal budget planner tools let you do this during the initial setup wizard. If it takes more than 15–20 minutes, you’re overcomplicating it.

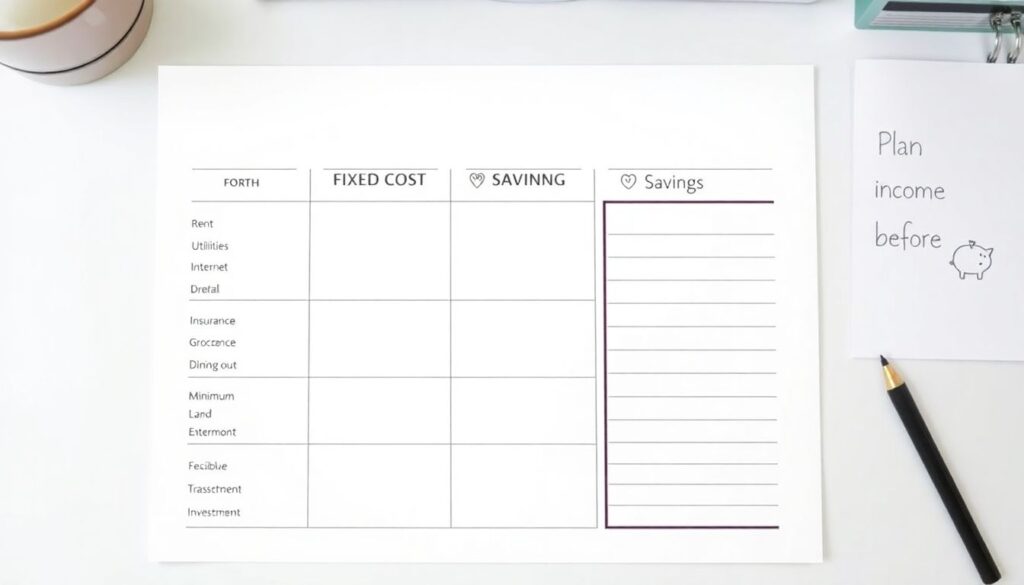

Method 4: One-page monthly budget that fits on your phone screen

Instead of a massive spreadsheet, make a one-page plan for the upcoming month before the money arrives. Take your expected income and split it into three blocks: fixed costs, flexible spending, and savings. Fixed costs are boring but predictable: rent, utilities, internet, insurance, minimum loan payments. Flexible is everything that can be adjusted week to week: groceries, cafes, clothes, transport, fun. Savings and debt prepayments go last, but you set them aside first. The genius of this method is that your entire month lives in one simple picture, not in 12 tabs of a complex file. You can do it on paper, in a notes app, or directly in an online budgeting tool to track spending that you actually understand.

Your rule of thumb: if your plan doesn’t fit on one screen of your phone, shrink the number of categories.

Technical block: numbers that show if your budget is “leaking”

– Housing (rent + utilities) over 40–45% of net income = high risk zone

– High-interest consumer debt (credit cards, payday loans) over 20% of income = emergency to fix

– No emergency fund and less than 5% going to savings = vulnerable to any shock

– Subscriptions over 5–7% of income = likely paying for things you forgot

Use these as alarms, not as reasons to panic. They tell you where to look first.

Method 5: Kill silent leaks — subscriptions, fees, and “small” habits

Silent leaks are the expenses you don’t emotionally feel. No one feels a $4.99 subscription or a $3 service fee. But multiply that over 12 months and across several services, and suddenly it’s $400–$600 a year. A 2022 report by C+R Research found that 42% of people continue paying for at least one subscription they no longer use. Financial coaches often start with a “subscription audit”: once a quarter, go through your bank statement and app store purchases, list every recurring charge, and ask: “If this started today, would I sign up?” If the answer is “no” or “meh”, cancel it. That five-minute act can free up more than any complicated investment strategy at your income level.

Another classic leak: daily habits. One coffee for $4 and one snack for $3 every workday is about $140 a month, or $1,680 a year. If you like that habit – keep it. But do it consciously, not on autopilot.

Expert tip: “replace, don’t forbid”

Behavioral economists note that bans rarely work long-term. Instead of “no coffee”, try “three café coffees a week, two from home”. Instead of “no delivery”, try “delivery only on weekends”. You still enjoy the habit, but you reduce the frequency by 30–50%, and your spending follows.

Method 6: Automate the boring parts so you don’t rely on willpower

Relying on willpower is like relying on good weather. Some days it’s there, some days it absolutely isn’t. That’s where automation comes in. Set an automatic transfer to your savings account the day after payday, even if it’s just $30–$50. Automatically pay your main bills to avoid late fees. Lock your credit card for online purchases and use a virtual card with a strict monthly limit. These small systems mean you don’t have to make 100 “smart” decisions; you make a few smart setups and let them run. It’s the same logic behind retirement plans that auto-enroll employees: when saving becomes the default, participation rates jump dramatically.

Think of automation as rails for your money: they guide the flow without you steering every second.

Technical block: basic automation setup

– Automatic savings: 5–10% of income to a separate account on payday

– Card limits: set a monthly online spending cap (e.g. $150)

– Bill autopay: at least for rent, utilities, phone, and insurance

– Alerts: push notification for any expense over a custom amount (e.g. >$50)

Most banks and monthly budget tracking software already support these features. Use them, or you’re leaving easy money on the table.

How to manage monthly expenses and save money without turning your life into an Excel sheet

You don’t have to become a different person to get control over your cash. Choose one tracking method (paper, app, or one-page plan) and one automation step, and run them for 30 days. That’s it. After a month, sit down with your numbers for 20 minutes. You’ll probably spot 2–3 obvious leaks totalling $50–$200 a month. Cancel or reduce them, and redirect that money to a small emergency fund or a specific goal like “trip fund” or “buffer for car repairs”. Many people discover that once the first $500–$1,000 safety cushion is there, anxiety about money drops заметно, и становится проще принимать взвешенные решения, а не тянуться к кредитке при каждом чихе.

Over time you can layer more: try one of the best expense tracking apps, experiment with different personal budget planner tools, or move your whole system into an online budgeting tool to track spending in real time. But start simple: watch where your money actually goes, patch the obvious leaks, and let small, boring systems quietly improve your finances month after month.