Start here: what “capital gains tax on crypto” really means

Before you try to minimize anything, you need to know what you’re actually minimizing.

Very short version:

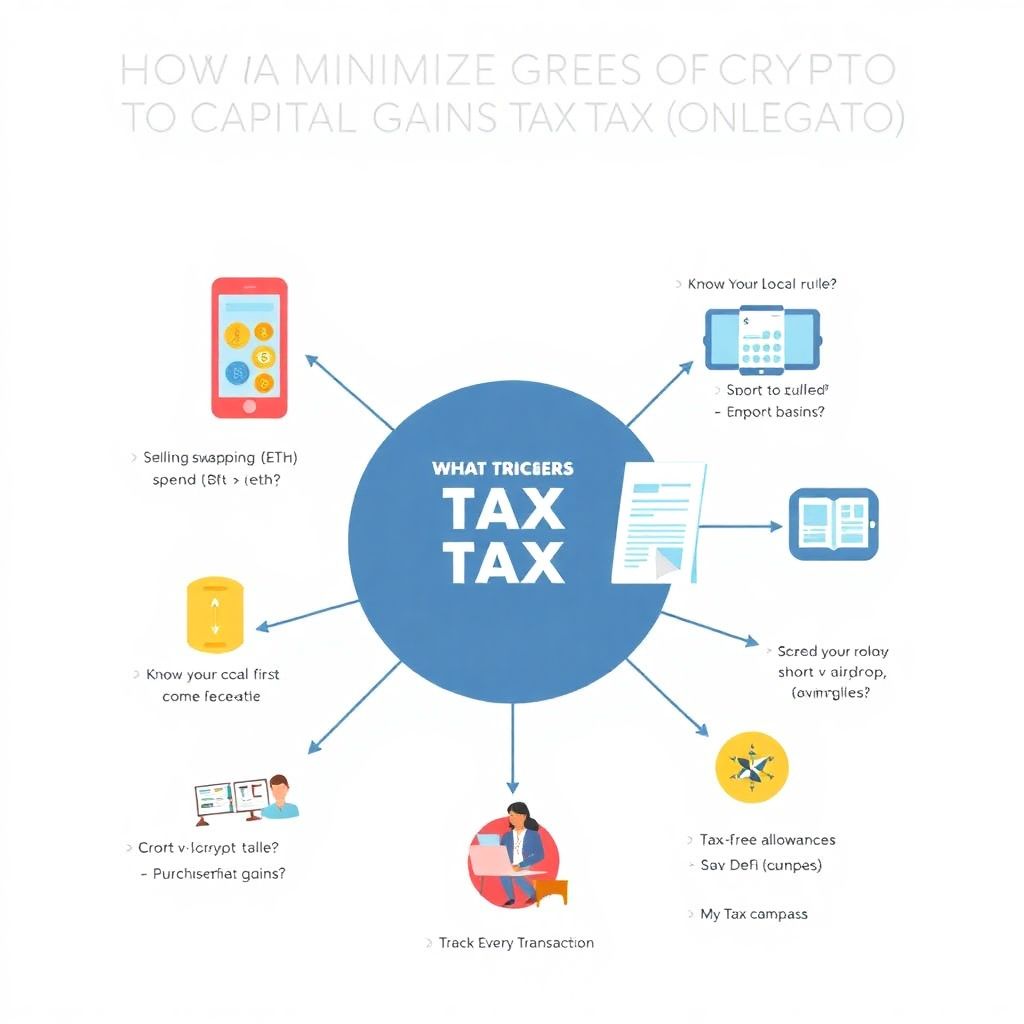

– When you sell, swap, spend, or sometimes even gift crypto, you may trigger a taxable event.

– Profit = selling price – purchase price (cost basis).

– That profit is a capital gain.

– Depending on how long you held the asset and where you live, it’s usually taxed as income or capital gains.

If you’re looking for how to avoid capital gains tax on cryptocurrency legally, the key word is “legally”. You’re not trying to hide trades; you’re trying to shape them so the tax bill is smaller, more predictable, and easier to pay.

> Quick disclaimer: this is education, not personal tax or legal advice. Rules vary a lot by country and even state. Always verify with a professional who understands crypto in your jurisdiction.

—

Step 1. Map your tax rules before you trade (not after)

Most people start thinking about taxes in April. That’s like learning the rules of chess after losing your queen.

Take one evening to answer these questions for your country:

– Are crypto-to-crypto swaps taxable? (e.g., BTC → ETH)

– Is paying for goods or services with crypto a taxable disposal?

– Do you have different rates for short-term vs long-term gains?

– Are there tax-free thresholds or allowances?

– How is staking, airdrops, mining, and yield farming treated?

Then write down three sentences:

1. “A taxable event happens when I _______.”

2. “My lowest tax rate applies when I hold more than _______.”

3. “My tax-free allowance / lowest-bracket room is roughly _______ per year.”

This becomes your personal “tax compass.” Every trade should respect it.

—

Step 2. Track everything from day one (and automate it)

If your records are a mess, your tax bill will be worse than it needs to be.

What to track for each transaction

At minimum:

– Date and time

– What you gave and what you received

– Quantity and unit price in your local currency

– Fees paid

– Purpose (trade, payment, transfer, airdrop, reward, etc.)

If you use many exchanges, wallets, and chains, do not try to maintain this in a homemade spreadsheet unless you’re extremely organized and doing very low volume.

Instead, pick a tool. When you search for the best crypto tax software for capital gains reporting, focus less on marketing and more on:

– Does it support all the chains, DEXes, and NFTs you actually use?

– Can it import automatically via API and xPub, not just CSVs?

– Does it handle staking, liquidity pools, bridges, and wrapped tokens correctly?

– Can you easily fix errors and assign missing cost basis?

The earlier you connect everything, the cheaper and cleaner your reports will be.

—

Step 3. Learn how to calculate and reduce crypto capital gains taxes

This sounds boring, but once you understand the levers, you can get creative without breaking laws.

Basic calculation logic

A simple mental model:

– For each disposal, you have:

– Proceeds: what you got (in fiat terms)

– Cost basis: what you originally paid for the crypto you’re selling

– Gain or loss: proceeds – cost basis

Two common accounting methods (check what’s allowed where you live):

– FIFO (First In, First Out) – you sell your oldest coins first.

– Specific identification / HIFO – you intentionally sell lots with the highest cost basis first to minimize gains.

Understanding how to calculate and reduce crypto capital gains taxes is partly about choosing the right lots to sell and timing those sales.

—

Step 4. Design your personal crypto tax planning strategies

Now the fun part: crypto tax planning strategies for minimizing capital gains that are still on the right side of the law.

Below are both standard and more unusual approaches.

1. Stretch your holding period on purpose

In many countries:

– Hold less than X months → higher short-term rate

– Hold more than X months → lower long-term rate

So instead of “I’ll sell when it hits $X,” shift to:

“I’ll start selling after I’ve crossed the long-term holding period, unless the market is going crazy.”

Tiny tweak; big savings.

Mistake to avoid:

Panic-selling one week before your holding period turns long-term, creating a big, unnecessarily expensive gain.

—

2. Use “tax-loss harvesting” — but do it smart

If some positions are in profit and others are deep in the red, you can:

– Realize (sell) some losers to offset your realized winners.

– In some jurisdictions, excess capital losses can offset other income up to a limit or be carried forward.

Unconventional twist:

Instead of waiting until December, set a rule like:

– “Once a month, I check my portfolio and realize some losses if:

– The project is something I no longer believe in and

– I have gains elsewhere this year.”

This spreads your adjustments through the year, which is psychologically easier and usually more effective.

Warning: Some countries have wash-sale rules that punish selling and immediately rebuying just for tax purposes. Many don’t explicitly cover crypto yet, but copying stock rules blindly can be risky. Respect both the letter and spirit of the law.

—

3. Swap “high-gain coins” into “low-gain coins” strategically

Non-obvious idea:

– Let’s say Coin A has huge unrealized gains. Coin B is roughly break-even or a small loss.

– You want to reduce concentration risk in Coin A but don’t want a massive tax hit.

A more nuanced move:

1. Sell part of Coin A gradually over time, staying within a comfortable tax bracket each year.

2. Pair some of those gains with realizing losses or small gains on Coin B at moments that keep your net annual gain in a target range.

3. Rebuild positions through fresh deposits rather than heavy in-year rotations.

The goal isn’t “zero tax this year.” It’s smooth, predictable tax over multiple years instead of one giant spike.

—

4. Turn some trades into “non-taxable life improvements”

Depending on your jurisdiction, there may be ways to:

– Use tax-advantaged accounts for certain crypto exposures (ETFs, trusts, or derivatives inside a retirement account, for example).

– Shift some returns into long-term savings vehicles instead of constantly recycling them in a trading account.

Unconventional angle:

Instead of trying to trade every wiggle, assign some positions to “I will never sell this in my personal name; it’s for retirement only.” Put those into the most tax-efficient wrapper available in your country, even if that wrapper has fees or limited asset choice.

You may sacrifice some flexibility but gain smoother compounding without yearly capital gains friction.

—

5. Relocation and legal entity structuring (only if it really fits your life)

A lot of people fantasize about moving to a “crypto tax haven.” Sometimes it’s smart; often it’s overkill.

More realistic, nuanced approach:

– If you were already considering moving for work, safety, or lifestyle, then add tax rules into your decision.

– If your trading looks more like a business (large volume, systematic strategies, DeFi operations), discuss with a professional whether a legal entity (company, fund structure, etc.) could improve both tax and liability.

However:

– Don’t move countries just to dodge taxes unless everything else about the move also makes sense for your life.

– Don’t open complex offshore structures you don’t fully understand; compliance costs and risks can destroy the supposed benefit.

This is where a crypto tax accountant for capital gains optimization can save you from expensive overengineering or from missing a simple, more appropriate structure.

—

Step 5. Tame DeFi, NFTs and “weird” income sources

This is where most people accidentally create tax chaos.

Staking, yield farming, lending

Key questions to clarify (locally):

– Are staking or farming rewards taxed as income when received, or only as capital gains when sold?

– Are gas fees and protocol fees deductible? When?

– Do rebase tokens or auto-compounding vaults create reportable events?

Unconventional but helpful practice:

– Treat each new protocol like a mini-business you’re opening. Before you deposit:

– Skim their docs.

– Check how previous users report similar rewards in your country.

– Decide in advance how you’ll categorize the income and track it.

Write that decision in a short note to your future self. When you do your return months later, you’ll be grateful.

—

NFTs and meme coins

These can be a tax nightmare because:

– People jump between wallets, bridges, and chains without notes.

– They forget the original cost basis (especially for absurdly cheap mints).

– They pay huge gas fees they never record properly.

Try this:

– Have a separate wallet just for “speculative / casino” stuff.

– Connect that wallet to your tax software as a distinct account.

– Once a month, export a snapshot and quickly label:

– Deads (worthless, illiquid)

– Keeps (long-term holds)

– Exits (to be sold this tax year if convenient)

This keeps your long-term, high-conviction holdings mentally and administratively separate from your experiments.

—

Step 6. Turn your tax report into a feedback loop

Your yearly return is more than a chore; it’s a free diagnostic.

When you run the numbers:

– Which trades produced most of your gains?

– Which habits produced most of your losses and fees?

– How much did you pay in tax per $1 of net profit?

If you notice, for example, that short-term scalping produced wild stress and a high tax bill, while simple long-term holdings delivered most of the profit, that’s a powerful nudge to adjust strategy.

Unconventional trick:

Once a year, write a one-page “Investor’s Tax Letter to Myself”:

– What worked (tax-wise)?

– What was a disaster?

– What rules do I want for next year? (e.g., “No more than X disposals per month,” “Never rotate whole portfolio in a single quarter,” etc.)

Stick to it for 12 months and compare results.

—

Step 7. Know when DIY is over and you need help

Doing everything yourself makes sense at the beginning. But once your trades, DeFi activity, or portfolio size become significant, a good professional can more than pay for themselves.

Signs you might want help:

– You’re active on multiple chains and protocols and feel lost.

– You’re considering moving countries or starting a legal entity.

– You’re nervous that a past year’s filing may be wrong.

– You’re spending more than a couple of weekends per year wrestling with spreadsheets.

When talking to a specialist:

– Ask specifically about their experience with on-chain data.

– Check how they handle missing records or dead exchanges.

– Discuss not just last year’s filing, but a multi-year roadmap for your crypto activity.

Use them not only to file forms, but to refine your strategy for the next few years.

—

Common mistakes that silently inflate your crypto tax bill

A quick checklist of what to avoid:

– Ignoring small trades and airdrops “because they’re tiny” – they pile up and create messy, sometimes expensive surprises.

– Confusing transfers with disposals – moving your coins between your own wallets is usually not taxable, but must be recognized as transfers, not trades, in your software.

– Overtrading for excitement – lots of small short-term gains can put you in a higher bracket than a few big, well-timed moves.

– Forgetting to account for fees – fees increase your cost basis or reduce your proceeds; ignoring them makes gains look bigger than they are.

– Waiting until tax season to organize – by then, prices, memos, and even platforms may have disappeared.

Build a habit of checking your tax dashboard monthly, not yearly. Five minutes now can save hours – and a chunk of money – later.

—

Putting it all together

Managing and minimizing capital gains taxes on crypto profits isn’t about magical loopholes. It’s about:

– Knowing your local rules before you push buttons.

– Tracking every move with tools that understand crypto.

– Planning your disposals like an investor, not reacting like a gambler.

– Using legal tactics – holding periods, loss harvesting, bracket management, and structuring – deliberately, not out of panic.

– Turning your yearly tax report into a strategy document, not just paperwork.

Handle those pieces well, and you won’t just lower your tax bill. You’ll probably become a calmer, more profitable crypto investor in the process.