Why mixing student loans and crypto even makes sense

Paying off debt and buying volatile assets sounds contradictory, but in reality people do it all the time through 401(k) contributions, brokerage accounts and side investments. Crypto is just a higher‑beta version of that idea. The real problem isn’t “crypto vs loans”, it’s absence of structure. If you don’t have a clear student loan payoff plan with crypto investments integrated into a cash‑flow system, you end up making emotional decisions every time the market pumps or your servicer emails you. So let’s build a framework that tells you exactly what each dollar does: how much goes to minimums, how much accelerates principal, and how much you can risk in digital assets without sabotaging your future self.

Step 1: Map your liability profile like an analyst

Before asking how to pay off student loans fast while investing, you need a clean data set. Treat your loans like a mini corporate balance sheet. Create a simple list with loan type, balance, interest rate, monthly minimum, and whether it’s federal or private. Now calculate a weighted average interest rate and your total mandatory payment. This gives you your “debt cost of capital”. Compare that to a realistic—not fantasy—expected return for a diversified crypto portfolio over multiple years, adjusted for risk. Once you see that some loans cost you 7–9% after tax while Bitcoin might be −40% in a bad year, it becomes obvious why you can’t blindly shovel everything into tokens and hope it works out.

- List every loan with rate and balance

- Tag loans as high‑rate (>6%), medium (3–6%), low (<3%)

- Note federal protections: income‑driven plans, forbearance

- Identify which loans are candidates for aggressive payoff

Step 2: Define your “must survive” money

You can’t balance student loan repayment and cryptocurrency investing if rent is unstable, cards are maxed, and you have zero cash buffer. First, lock in a bare‑bones survival budget: housing, food, transport, insurance, minimum payments. This is non‑negotiable cash flow. Next, build a small emergency reserve, typically 1–3 months of core expenses in a boring high‑yield savings account. Only when these two layers are funded do you have “risk capital”. This structure prevents you from rage‑selling Bitcoin at a 60% drawdown just to cover a car repair. A lot of people skip this boring step, then blame “crypto” instead of acknowledging they were using speculative assets as a checking account substitute.

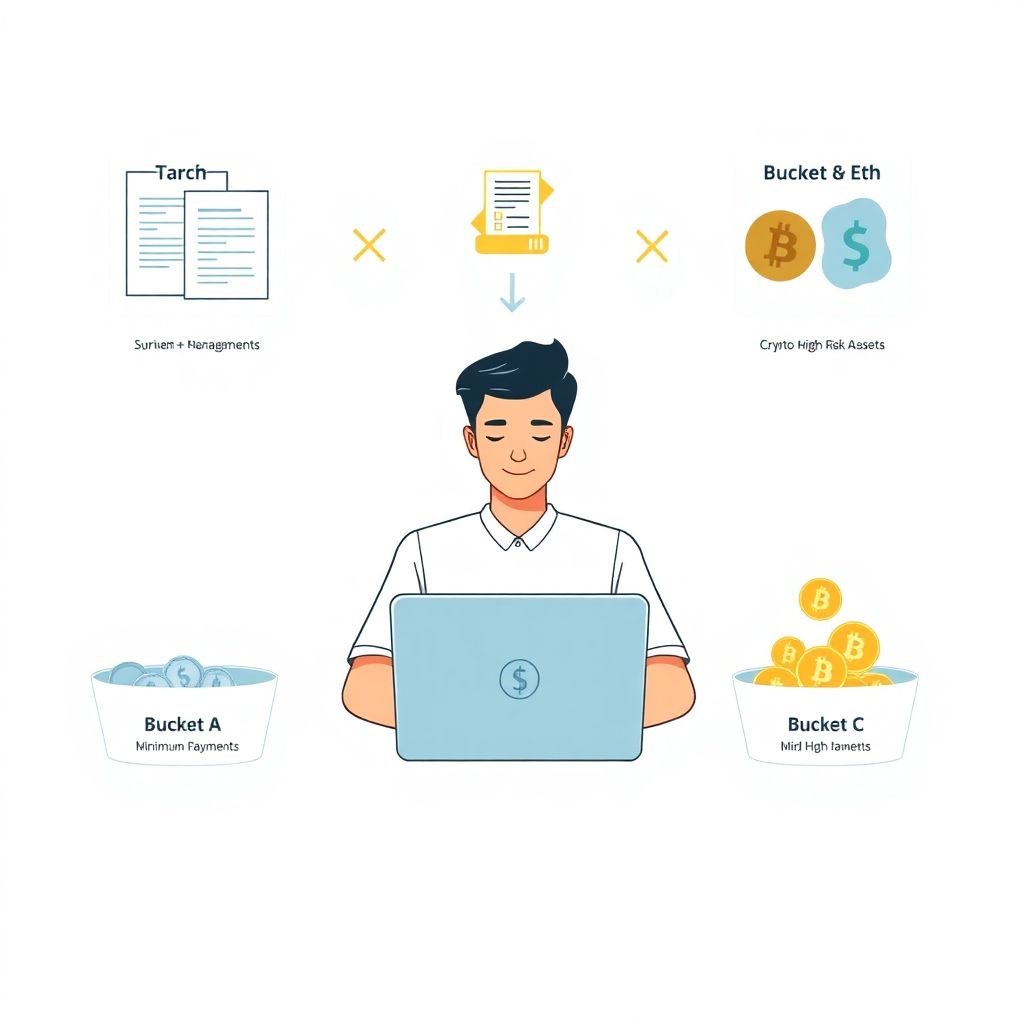

Step 3: Create the 3‑bucket cash‑flow system

Now to the best strategy to pay student loans and invest at the same time without chaos: a three‑bucket structure tied directly to each paycheck. Bucket A is obligations: all minimum payments on loans plus essentials. Bucket B is acceleration: extra principal payments targeted at your highest‑rate loans. Bucket C is “high‑volatility growth”, where crypto lives alongside any other speculative assets. Decide in advance a fixed percentage of net income for each bucket—for example 60% to A, 25% to B, 15% to C. Automate transfers on payday: one to your loan servicer for extra principal, one to your exchange or crypto on‑ramp. The rule is simple: you’re allowed to adjust allocations quarterly, not impulsively after a pump or crash.

- Bucket A: survival + minimum payments

- Bucket B: extra debt reduction on the highest APR loan

- Bucket C: crypto and other high‑risk assets

- Rebalance percentages every 3–6 months, not every news cycle

Step 4: Decide your priority using an interest vs risk test

The recurring dilemma is: should I pay off student loans or invest in crypto first? There’s no universal answer, but you can use a simple decision rule. If your highest‑rate loan after tax costs more than a conservative expected return on a diversified crypto basket (not your dream bull‑run scenario), debt gets priority in Bucket B. If your loans are low‑rate federal with strong protections and you work in a field with potential loan forgiveness, it can be rational to keep them on a long amortization schedule while routing more to Bucket C. The key is risk‑adjusted return: a guaranteed 7% saved on interest is mathematically superior to a highly uncertain 15% expected gain with huge drawdowns that can take years to recover.

Step 5: Build a rules‑based crypto allocation

To make how to balance student loan repayment and cryptocurrency investing practical, you need quantified constraints. Start by capping your total crypto exposure as a percentage of net worth—say 5–15% depending on risk tolerance and job stability. Within that cap, split between large‑cap layer‑1 assets (e.g., BTC, ETH) and any higher‑risk altcoins. Use dollar‑cost averaging: buy on a fixed schedule regardless of price, instead of chasing green candles. Avoid leverage and complex derivatives while you’re still in repayment mode; your human capital is already leveraged by debt. Most importantly, never, under any circumstances, fund crypto buys with new credit card debt or personal loans. If you can’t buy from free cash flow, you can’t afford the position.

- Set a maximum crypto share of net worth (hard cap)

- Automate recurring buys instead of manual “FOMO” entries

- Favor BTC/ETH over illiquid micro‑caps while in heavy debt

- Disable margin and options until loans are under control

Step 6: Design an actual student loan payoff plan with crypto in mind

Let’s turn this into numbers. Assume you clear $4,000 per month after tax. Your survival and minimums (Bucket A) are $2,400. You decide on 25% ($1,000) to Bucket B and 15% ($600) to Bucket C. You target your highest‑rate 8% private loan with the entire $1,000 as extra principal, while automatically dollar‑cost averaging that $600 into BTC and ETH every month. Once the 8% loan is gone, you don’t instantly upgrade your lifestyle. Instead, you temporarily redirect most of that $1,000 into a mix of slightly more crypto and faster payoff of the next loan, maintaining the same overall savings rate. Over several years, this compounding discipline crushes principal while your crypto stack grows in the background.

Step 7: Use market cycles intelligently, not emotionally

Markets move faster than loan servicers. When crypto has a parabolic year and your portfolio suddenly doubles, you re‑run the math. Lock in some gains by trimming positions back to your pre‑defined net‑worth cap and apply the freed‑up capital to debt. That might mean liquidating a portion of profits to completely wipe out a mid‑rate loan a few years early. Conversely, in a brutal bear market you do not turn off your extra loan payments to “average down harder”. You stick to your buckets, maybe even tilt slightly from Bucket C toward B if job risk rises. The plan isn’t about perfect timing; it’s about preventing euphoric over‑exposure and panic‑driven capitulation that can wipe out both your balance sheet and your sanity.

- Recalculate net‑worth allocation annually or after big moves

- Skim profits above your crypto cap and send them to loans

- Resist the urge to cut extra payments during drawdowns

- Only change rules in calm periods, never mid‑crash or mania

Step 8: Automate, monitor, and iterate like a systems engineer

None of this works if it lives only in your head. Put every element on rails: automatic loan payments (minimum plus fixed extra), recurring crypto buys, and scheduled check‑ins. Once a quarter, review three metrics: total principal remaining, effective interest saved versus original amortization, and current crypto allocation versus your cap. Adjust Bucket percentages if your income changes materially or your risk tolerance shifts, but do it with intention, not impulse. Over time you’ll notice something: the initial question of how to pay off student loans fast while investing stops feeling like a tug‑of‑war. You’re just executing a repeatable process where debt shrinks on schedule while your exposure to upside assets grows under strict, quantified constraints.