Why budgeting prize money and sponsorships feels so tricky

If your income comes from tournaments, appearance fees, brand deals or creator sponsorships, your cash flow probably looks like a rollercoaster. One month you land a big win, the next month is almost empty. That’s exactly why financial planning for athletes with prize money and sponsorships needs a different playbook than a normal 9‑to‑5 salary.

Over the last three years (2022–2024), industry reports have shown three clear trends:

– Total global sports sponsorship spending has steadily increased each year, driven by social media reach and influencer marketing.

– More athletes and creators are earning *some* money from brands, but average income is still highly uneven and often seasonal.

– Tax agencies in the US, UK and EU have published more guidance on digital and cross‑border earnings, which means less “gray area” and more need for proper records.

Exact numbers vary by source and country, but the direction is consistent: more deals, more types of income, more tax rules. Which means: you can’t “wing it” anymore.

Let’s unpack how to budget when your money shows up in spikes instead of smooth monthly paychecks.

—

Key terms: what are we even budgeting?

Prize winnings

Prize winnings are payouts you get from competitions or contests:

– Tournament prizes (sports, esports, poker, chess, etc.)

– Bonuses for rankings, titles or MVP awards

– Performance‑based bonuses from teams or leagues

Crucial point: in many countries, prize money is taxable income, sometimes with withholding at the source, sometimes not. That’s where tax planning services for prize money and sponsorship income become important, especially if you compete in multiple countries.

Sponsorships and endorsements

Sponsorship / endorsement income usually includes:

– Flat monthly retainers from brands

– Per‑post or per‑video payments

– Affiliate commissions and discount‑code revenue

– Royalties from merchandise or co‑branded products

– Appearance fees for events, signings, streams

The tricky part is that even sponsorship deals, which feel “stable”, can stop suddenly: brands shift budgets, campaigns end, performance drops. So this is still variable income, not a true salary.

Irregular vs. unstable income

These two are not the same:

– Irregular income – doesn’t arrive at the same time or in the same amount every month (your situation).

– Unstable income – genuinely at risk of disappearing entirely (e.g., one‑off viral sponsorships, a single big tournament win).

When people search how to budget irregular income from winnings and sponsorship deals, what they really need is a system that treats irregular and unstable money differently.

—

Simple mental model: your “boring salary” vs. your “spikes”

Imagine your total income as two separate streams:

1. Base income – what you can *reasonably* expect in an average bad‑to‑okay year

2. Spike income – the extra from big wins, surprise bonuses, viral brand deals

Here’s a text‑style diagram to visualize it:

> Diagram: Income layers

>

> [ Spike Income: big wins, unexpected deals ]

> ↑

> [ Base Income: minimum realistic yearly total ]

You build your budget only on the base layer, then assign a job to every future spike *before* it hits your account (debt, taxes, investing, big goals).

—

Step 1. Calculate your realistic base income (using a 3‑year view)

To get that base layer, use the past three years as your data set (2022, 2023, 2024 if you’ve been active that long).

1. Add up all your net income per year (after platform fees and team splits, before personal taxes).

2. For each year, note:

– Total from prize winnings

– Total from sponsorships and other brand work

3. Drop the best year (the outlier spike).

4. Take the lower of the remaining two years.

That lower figure is your conservative base annual income.

If your career is newer than three years, be even more conservative: assume you’ll earn 70–80% of your last 12 months as your base. Over the last three years, survey data from creator‑economy platforms has consistently shown high income volatility: large shares of full‑time creators and athletes report that a single month can account for a big chunk of their yearly earnings. That’s why you want to under‑promise and over‑deliver to yourself.

Convert that base annual number into a monthly planning number by dividing by 12. That’s your “boring salary” for budget purposes.

—

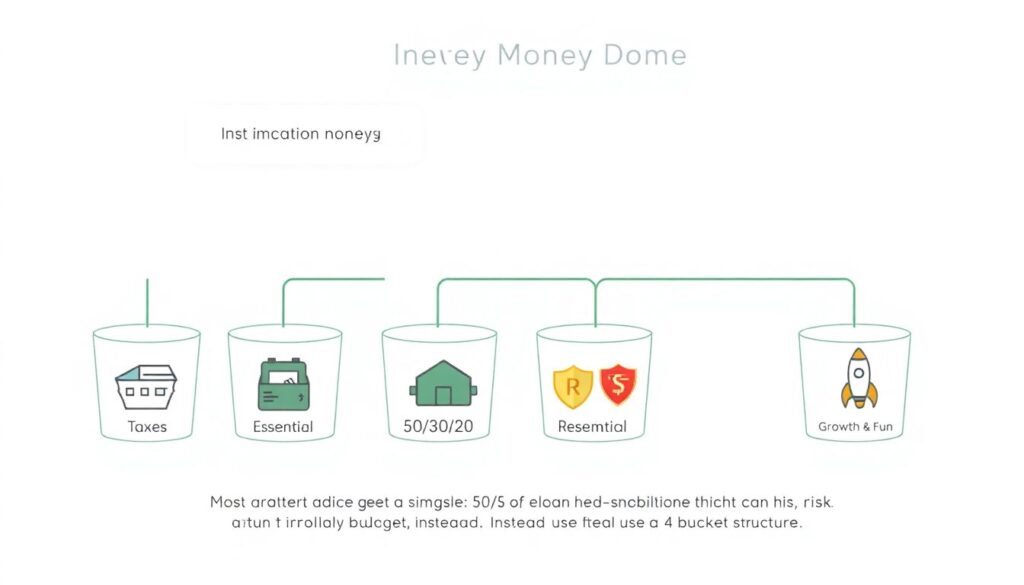

Step 2. The 4‑bucket budget specifically for variable prize and sponsor money

Most traditional advice tells salary earners to use a simple 50/30/20 budget. With your income pattern, that can be dangerous. Instead, try this four‑bucket structure:

> Diagram: 4‑bucket flow

>

> Incoming Money → [Taxes] → [Essentials] → [Safety / Reserves] → [Growth & Fun]

Here’s how it works.

Bucket 1: Taxes (non‑negotiable)

Every time money hits your account—prize or sponsorship—move a percentage into a separate tax account you never touch for spending. Think of it as money that was never truly yours.

Because tax rules have tightened for cross‑border payments and digital income between 2022 and 2024, there’s more risk of under‑withholding or late filing. Many pro athletes and influencers now use tax planning services for prize money and sponsorship income just to avoid surprise bills and penalties.

Rough guideline (very general; real rates depend on your country and deductions):

– Set aside 25–35% of each payment for national income tax.

– If you’re self‑employed, add a bit more to cover social contributions where relevant.

When a big win lands, treat taxes first, not last.

Bucket 2: Essential living expenses

These are the things that keep you alive and able to perform:

– Rent / mortgage

– Food and basic supplies

– Utilities, basic phone plan, transport

– Insurance (health, disability, liability, sometimes equipment)

Design your lifestyle so 100% of these essentials are covered by your base income number, not by your best‑case scenario. If you’re spending spike money on rent, you’re gambling your housing on performance.

Bucket 3: Safety reserves (your shock absorber)

This is your buffer against dry months:

– Emergency fund: usually 3–6 months of essential expenses, but for very irregular careers, 6–12 months is safer.

– Seasonal / off‑season fund: if your sport or content niche is seasonal, build a separate pot to cover planned low‑revenue periods.

Over the last three years, multiple athlete unions and player associations have reported that a significant share of younger pros struggle financially within 3–5 years of starting their careers, often due to lack of reserves and sudden injuries or non‑renewed contracts. A fat safety bucket is less flashy than a new car, but it’s what keeps you in the game long‑term.

Bucket 4: Growth & fun (the reward zone)

Only after buckets 1–3 are funded do you:

– Upgrade lifestyle (nicer apartment, better car, travel)

– Invest in skill development, coaching, team staff

– Put money into longer‑term investments

– Spend freely on non‑essentials

This is where spike income mostly goes. It’s your reward for discipline earlier in the chain.

—

Step 3. Budgeting method that matches variable income

Standard monthly budgets assume you know your income in advance. You don’t. So flip the script: budget based on money already received, not on guesses.

Here’s a practical 5‑step method:

1. When money comes in, sort it into the 4 buckets immediately.

2. Cover essentials for the coming month or two first.

3. Top up the tax account to your target percentage if needed.

4. Add to safety reserves until your emergency / off‑season targets are reached.

5. Only then assign remaining cash to growth and fun.

This “cash‑on‑hand” approach has become more common among freelancers and creators, especially from 2022 onward, as more people rely on platforms and brand deals with uncertain payouts.

—

Tools: money management apps and professional help

Using apps that actually work for irregular income

Most banking apps assume a steady paycheck, but you need something more flexible. Many athletes and influencers now look specifically for money management apps for variable income from prizes and sponsorships that allow:

– “Envelope” or “bucket” style saving (for taxes, emergencies, goals)

– Easy tagging of income sources (sponsor A, tournament B)

– Exportable reports for accountants and tax filings

– Alerts when you’re dipping below critical reserve levels

Even if you just use a simple budgeting app plus a spreadsheet, set it up so it mirrors your 4‑bucket system.

When to bring in a human: advisors and accountants

If your annual earnings from sport + sponsors are moving into the mid‑five figures or higher (in your local currency), it’s usually time to get professional help.

Look for the best financial advisor for professional athletes and influencers you can reasonably afford—not the one with the flashiest sales pitch, but one who actually understands:

– International prize money rules

– Appearance fees, royalties, affiliate income

– Image‑rights structures (where legal and appropriate)

– Cash‑flow planning for short careers or highly volatile income

Combine that with a proactive accountant who can help with tax projections and cross‑border issues. Over the last 3 years, many high‑profile cases of unpaid taxes for digital creators have been publicized, often due to poor professional guidance or no guidance at all.

—

Examples: two athletes, two outcomes

Example 1: The “all‑in” spender

– 2022: Wins a big regional tournament, signs a one‑year sponsor deal.

– Buys a luxury car, upgrades to an expensive apartment, no tax or emergency fund.

– 2023: Underperforms, sponsor doesn’t renew, prize earnings drop.

– Suddenly can’t cover rent or car lease; owes a large tax bill from 2022 income.

– Has to borrow or sell assets at a loss just to stay afloat.

Outcome: lifestyle was built on spike income, not on a conservative base. No buckets, no buffer.

Example 2: The “boring on purpose” planner

– 2022: Strong year with prize wins + several sponsorships.

– Calculates a conservative base income using the 3‑year method and sets lifestyle below that.

– Uses each payout to:

– Move 30% to taxes

– Cover modest rent and living

– Build up 9 months of emergency + off‑season fund

– Only then upgrades equipment and takes a short vacation

– 2023: Results are weaker, two sponsors pause campaigns.

– Still covered: essentials + taxes + training costs, using savings built in 2022.

– 2024: Changes coach, invests in mental performance, returns to better form with a more stable sponsor mix.

Outcome: short slump, but no financial crisis. Budgeting system gave room to adapt and improve.

—

Numbers and trends from the last 3 years (2022–2024)

Without making up fake precision, here’s what public data and industry reports have broadly shown over the last three years:

1. Growth in sponsorship opportunities

– Global sports and influencer sponsorship spending has grown each year from 2022 to 2024, as brands shift budgets from traditional ads to creator and athlete partnerships.

– Even “micro‑athletes” and smaller creators are getting deals, but their earnings are more volatile and campaign‑based rather than long‑term.

2. Concentration of income at the top

– In many sports and creator platforms, a small percentage of top performers capture a very large share of total prize and sponsor money.

– Survey data from 2022–2024 consistently show that a majority of creators and lower‑rank pros earn irregular amounts that *don’t* match the public perception of big money.

3. Increased tax enforcement

– Revenue agencies in major markets have, over this period, issued clearer guidance about declaring income from streaming, platforms, foreign tournaments and online sponsorships.

– More cross‑checking between platforms, payment processors and tax authorities means under‑reporting is riskier now than it was before 2022.

4. Growing financial stress among young pros

– Players’ unions, Olympic committees and athlete welfare organizations have flagged rising financial stress, especially around:

– Paying taxes on time

– Managing sudden windfalls

– Planning for life after sport or content careers

The pattern is simple: opportunities are up, but so are the stakes if you mismanage cash.

—

Common mistakes to avoid with variable prize and sponsor income

Here are five errors that repeatedly show up when people ask how to budget irregular income from winnings and sponsorship deals:

1. Treating every sponsor deal like it’s permanent

Assuming your best year repeats forever leads to over‑committed fixed costs (huge rent, long‑term leases).

2. Ignoring taxes until the end of the year

This is how a great season turns into a disastrous spring when the tax bill arrives.

3. No separation between personal and “business” money

Mixing everything in one account makes it nearly impossible to track what’s actually happening.

4. Underinvesting in health, insurance and recovery

Short careers mean you’re one injury or burnout away from a revenue cliff.

5. Chasing status purchases instead of reserves

Cars, watches, and weekend blowouts instead of 6–12 months of living costs.

—

Step‑by‑step checklist to put this into practice

To wrap it up, here’s a concrete 7‑step action plan you can start this month:

1. Review your last 3 years of income (or as far back as you can).

Separate prize money, sponsor deals and other income.

2. Calculate a conservative base income.

Use the method from earlier and turn it into a monthly planning number.

3. Open at least two extra accounts.

One for taxes, one for emergency / off‑season savings.

4. Pick a budgeting tool or app.

Choose something that supports buckets or envelopes and works well as a money management app for variable income from prizes and sponsorships.

5. Design a 4‑bucket rule for every new payment.

Decide the percentages in advance (for example: 30% tax, 40–50% essentials, rest to reserves and growth/fun).

6. Set a reserve target and track progress.

Aim for at least 6 months of essential expenses saved; 9–12 months if your income is highly seasonal.

7. Book a session with a qualified advisor or accountant.

Even one meeting with a specialist in athlete/creator finances can save you years of mistakes.

—

Final thoughts

Your income might be unpredictable, but your system doesn’t have to be. With a clear base income number, a 4‑bucket structure, the right tools, and occasional help from professionals, you can turn volatile prize money and sponsorships into a livable, sustainable financial life.

You’re already used to training, tracking and adjusting in your sport or content niche. Budgeting this kind of income is the same skill set—just applied to money instead of performance.