Most people already understand risk and reward – just not from Wall Street. You’ve seen it in games: open a loot box, maybe you get a legendary skin, maybe you get junk. Investing works on the same logic, but with much higher stakes and far less glitter. Instead of skins, you’re dealing with rent money, retirement and real-world freedom. Below is a practical walkthrough that translates gaming intuition into real-life investing, with expert-style recommendations, concrete steps and a focus on index funds as a more reliable “upgrade path” than loot boxes.

—

From Loot Boxes to Index Funds: Why Your Gamer Brain Is Already Good at Finance

If you’ve ever hesitated before buying a loot box, you’ve already run a mental “risk vs reward” calculation. You asked yourself: how likely am I to get something useful, and is it worth my money and time? Real investing is the same idea, except it uses math, time and diversification instead of flashy animations and random number generators. Loot boxes concentrate risk into one random spin; broad index funds spread risk across hundreds or thousands of companies, turning wild swings into smoother progress over years. Understanding that difference is the starting point for building risk vs reward investment strategies that don’t feel like gambling and don’t depend on luck or hype.

—

Necessary Tools: What You Actually Need to Start

Digital and Financial Basics

To invest, you don’t need a suit, a finance degree or a huge paycheck. You need a few boring but powerful tools: a smartphone or computer, internet access, and a brokerage account or investing app that lets you buy index funds with low fees. This setup is your “game launcher” for finance. When you look up the best index funds for beginners, you’ll notice a pattern: low cost, broad market coverage and simple structure. Those characteristics do more for your long-term wealth than any hot stock tip. Treat fees like in‑game microtransactions: small individually, deadly over time if you’re not paying attention.

Knowledge and Mindset Stack

Hardware and apps are only half the toolkit. The more important tools are mental: patience, curiosity, and a basic understanding of how markets and compounding work. You don’t need to predict which company will be the next tech giant; you need to understand that owning a slice of many companies and holding them for years tilts the odds massively in your favor. Expert financial planners often say the winning combo is “a good plan you can stick to.” That means choosing safe long term investment options that match your personality, not the most aggressive strategy that looks impressive on paper but makes you panic during the first market drop.

Information Sources You Can Trust

In games, you eventually learn which streamers are skilled and which ones just shout over highlight clips. Finance content works the same way. You want sources that show data, explain risks and don’t promise guaranteed riches. Serious experts tend to be boringly honest: they talk about decades, not days; probabilities, not certainties. Before you commit money, get comfortable reading a basic fund factsheet, looking at fees (expense ratio), and checking whether a fund is diversified across sectors and countries. This small skill separates investors from speculators chasing the next loot box jackpot.

—

Step-by-Step Process: From Zero to Your First Index Fund

Step 1: Define Your Real-Life “Win Condition”

Every game has an objective: finish the campaign, reach top rank, collect all achievements. Investing needs the same clarity. Are you building a safety buffer for emergencies, saving for a down payment, or stacking wealth for retirement? Write down specific goals, rough timelines, and how much money you can realistically set aside each month. Expert advisors often start with what they call “goal-based planning” because it directly shapes how much risk makes sense. You wouldn’t take the riskiest loot box when you only have enough in‑game currency for one attempt; similarly, you shouldn’t bet rent money on volatile assets just because they might have higher returns.

Step 2: Learn How Risk and Reward Really Trade Off

In games, high-risk choices can be exciting: rush the boss with low health, or attempt a speedrun shortcut. In money terms, high risk means a real chance of losing significant value for long stretches. That’s why professionals emphasise understanding risk vs reward investment strategies instead of just chasing the highest historical returns. Low-risk assets like government bonds tend to move slowly but rarely implode, while stocks move more sharply but historically grow more over long periods. Index funds that track broad stock markets sit in a middle ground: they’re still risky in the short term but spread across many companies, which reduces the odds of catastrophic, permanent loss compared with betting everything on a single stock.

Step 3: Decide How to Start Investing With Little Money

Beginners often assume they need thousands to get started. Modern brokers and investing apps allow you to buy fractional shares of funds, so how to start investing with little money becomes surprisingly simple: pick a low‑fee index fund, automate a small monthly contribution, and increase it as your income grows. Many experts recommend starting even with tiny amounts just to build the habit, because behavioral patterns matter more than the size of your first deposit. Just like daily quests in games, consistent small actions compound over time. The important move is to cross the line from “I’ll invest someday” to “I invest every month, even if it’s modest.”

Step 4: Choose Vehicles – Index Funds, Mutual Funds, or Both

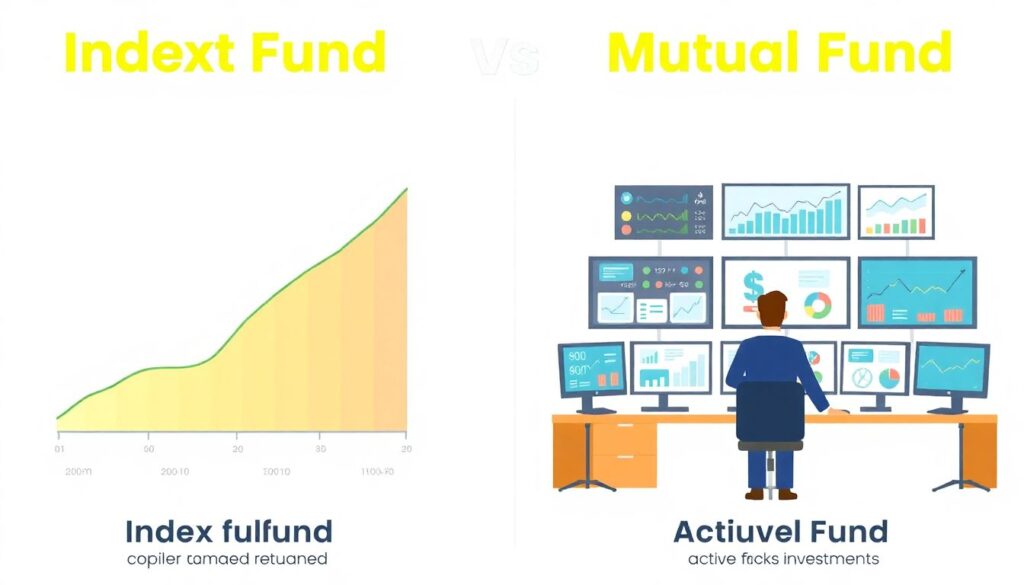

At some point you’ll see people compare index funds and mutual funds and wonder what the difference really means for you. In plain language: an index fund simply tries to copy a market index (like a broad stock market), while many mutual funds pay an active manager to pick specific investments. Index funds are typically cheaper and more transparent because they follow clear rules. Expert research over decades has shown that most active managers fail to beat simple index funds once you factor in fees and taxes. For a long-term, low‑maintenance approach, many financial planners point to broad, low-cost index funds as a core building block, adding a few specialized funds only if you fully understand why you want them.

Step 5: Build a Basic, Boring, Effective Portfolio

Once you’ve chosen your main fund or funds, the next task is to decide how much goes into what. A classic expert guideline is to combine a global stock index fund with a bond or cash-like fund. Stocks provide growth; bonds reduce fluctuations. Your age, income stability, and nerves determine the mix. Younger investors with decades ahead can usually afford more in stocks, while those nearing big goals might dial up bonds. The point is not perfection; it’s a simple structure that you can explain in one or two sentences and that you are willing to keep during both bull and bear markets. Clarity beats complexity when you want to actually stick to your plan.

Step 6: Automate and Ignore the Noise

After setup, the smartest move is often to get out of your own way. Automation is your ally: schedule monthly contributions, set a calendar reminder to check in once or twice a year, and otherwise treat the account like a retirement save file you don’t constantly reload. Seasoned professionals repeatedly warn that the worst returns usually come from people who jump in and out during every scare story or hype wave. Think of it this way: you don’t uninstall a game every time you lose a match; you keep playing, trusting that your long-run skill and strategy matter more than any single round.

—

Expert-Style Recommendations You Can Actually Use

Core Principles from Professional Investors

If you read what long‑term money managers, financial planners and academic researchers say, some themes repeat. First, diversification: owning many different companies and asset types reduces the damage from any single failure. Second, low fees: every extra percentage point in costs quietly erodes your eventual wealth. Third, time in the market: remaining invested for long periods has historically mattered far more than perfectly timing your entry or exit. These experts also insist on matching your investments to your tolerance for volatility; if you lose sleep when your account drops 10%, your mix is too aggressive, regardless of any theoretical advantages on a spreadsheet.

Why Index Funds Get So Much Praise

When professionals talk about the best index funds for beginners, they usually mean simple, diversified funds that track a broad market at minimal cost. Examples include total market or S&P 500 style index funds in the U.S., or global equity funds in other regions. The appeal is that you get instant access to hundreds or thousands of companies in one click, without having to become an expert stock picker. Legendary investors like John Bogle and Warren Buffett have repeatedly recommended broad index funds for most people because history shows how tough it is to consistently beat the market after fees. Instead of hunting for unicorns, you just own the whole herd and let global capitalism do the heavy lifting over decades.

Balancing Safety and Growth Like a Pro

Professional advisors don’t chase only maximum returns; they aim for the right balance between protecting capital and growing it. That’s where safe long term investment options such as broad bond funds, government securities and even high‑yield savings come in. These tools won’t make you rich quickly, but they keep your short‑term goals and emergency funds insulated from market storms. Experts typically separate money by time horizon: near‑term needs stay in safer assets, long‑term goals lean more on stocks and index funds. Copying this structure turns your finances into a set of clearly labeled “save files”: one for safety, one for growth, and less temptation to risk everything on speculative plays.

—

Using Gamer Logic to Understand Risk vs Reward

Loot Boxes vs. Owning the Whole Store

A loot box gives you a random roll from a limited pool of items. Buying an individual volatile stock is similar: maybe it moons, maybe it crashes. An index fund is closer to owning a share of the entire in‑game store: if some items flop, others sell so well that overall profits still rise. This is the heart of practical risk vs reward investment strategies: you cap how much any single bet can hurt you, but you still participate in the overall growth of businesses and economies. Instead of asking “Will this one company explode upward?” you ask “Is the global economy likely to grow over the next 20–30 years?” Historically, that second question has had a more reliable answer.

Understanding Volatility Without Panicking

Games teach you that sometimes you lose streaks, and it doesn’t mean you suddenly became terrible. Markets work the same way. Prices go up and down as news hits, interest rates change, or investors panic or celebrate. Experts treat this volatility as the “entry fee” for higher long‑term returns. The key is separating temporary drops from permanent damage. A well-diversified index fund may drop sharply during a recession, but if you stay invested, history shows recoveries have eventually followed. Owning a narrow, speculative bet that never comes back is different; that’s closer to burning money on a rigged loot box, hoping for a legendary that never appears.

—

Troubleshooting: Fixing Common Beginner Mistakes

Problem 1: Feeling Overwhelmed and Stuck at the Start

Many people get trapped at the research stage, bouncing between blogs, videos and conflicting advice. To get unstuck, constrain your choices: limit yourself to a small menu of diversified index funds and a reasonably priced bond fund. Experts often tell clients that the worst portfolio is the one that never gets implemented. If you spend six months debating between almost identical low-cost funds, you’re losing valuable compounding time. A practical approach is to pick a sensible option, start small, and grant yourself permission to adjust later as you learn, rather than delaying until you feel “fully ready” (a day that rarely arrives).

Problem 2: Panicking During Market Dips

The first time your account drops noticeably, your brain screams that you made a huge mistake. In that moment, your emotional software is running a “fight or flight” script, not a rational analysis. Seasoned professionals prepare for this in advance with written rules: how much you’ll invest, how often you’ll rebalance, and under what conditions you’d actually change your allocation. If you feel close to panic, experts suggest doing nothing immediately, reviewing your original plan, and comparing current declines to historical drawdowns in similar funds. Often you’ll see that what feels unprecedented has, in fact, happened many times before – and markets ultimately recovered. If you truly cannot handle the swings, that’s valuable data to shift toward a more conservative mix, not a cue to abandon investing altogether.

Problem 3: Overtrading and Chasing Hype

Switching funds constantly, jumping to whatever was hot last quarter, is the financial equivalent of endlessly rerolling characters instead of sticking with one and improving. Data from brokerage firms show that frequent traders often underperform simple buy‑and‑hold investors because they buy high and sell low, driven by emotions and news cycles. A useful troubleshooting move is to set a minimum holding period for each new investment – for example, promising yourself you won’t touch a core index fund for at least five years unless your life situation changes drastically. This small rule adds friction to impulsive decisions and keeps your attention on long-term performance rather than daily charts.

Problem 4: Not Knowing When Professional Help Makes Sense

DIY works for many, but not everyone loves diving into financial details. Good advisors can add value by clarifying goals, optimizing taxes, and acting as a “behavioral bodyguard” when markets get rough. If your situation is complex – multiple income streams, business ownership, large inheritances, or cross‑border issues – consulting a fee‑only planner may save you more than their cost. Experts in this field stress that the relationship should be transparent: you understand how they’re paid, what they’re doing, and how their recommendations align with your goals, not theirs. If an advisor pushes opaque products with high commissions, that’s a strong signal to walk away.

—

Putting It All Together: Turning Random Chance into a Long-Term Strategy

You already live with risk and reward every day: picking a career, moving cities, trying new projects. Games simply make that trade‑off more visible. Real-life investing is about taking that intuition and layering on structure, data and time. Instead of throwing cash at financial loot boxes – meme stocks, get‑rich‑quick schemes, opaque “opportunities” – you use simple tools like broad index funds, clear goals and automated contributions to let probability work in your favor. Experts who manage money for decades agree on the fundamentals: diversify widely, keep costs low, stay invested for the long haul and align your strategy with your real life, not with someone else’s highlight reel. If you treat your finances with the same focus you bring to mastering a complex game, your future self gets to enjoy the ultimate upgrade: genuine financial independence, earned through consistent, thoughtful play rather than one lucky drop.