Historical Context: The Evolution of Emergency Savings

Origins and Shifts in Financial Preparedness

The concept of emergency savings has evolved significantly over the past century. Initially, personal finance advice in the early 20th century emphasized frugality and self-reliance, often within the context of agrarian or industrial economies. However, the Great Depression of the 1930s marked a turning point, highlighting the necessity of financial buffers. In the aftermath, households became more attuned to the idea of precautionary savings. Fast forward to the 2008 global financial crisis, and again during the COVID-19 pandemic, the importance of emergency funds became starkly apparent. These periods of economic instability underscored how volatile job markets and health risks can destabilize even financially sound households. Recognizing this historical trajectory helps frame why emergency fund strategies are not merely financial advice but a vital component of economic resilience.

Fundamentals of Emergency Fund Planning

Core Principles and Financial Benchmarks

When exploring how to build an emergency fund, the foundational principle is liquidity. Unlike investments tied up in stocks or retirement accounts, emergency funds must be readily accessible. Financial advisors typically recommend setting aside three to six months’ worth of essential living expenses. This range accounts for variations in job security, health coverage, and personal risk tolerance. The best ways to save for emergencies involve automating deposits into high-yield savings accounts, avoiding high-risk or illiquid assets, and clearly defining what qualifies as an emergency. It’s crucial to separate these reserves from regular savings or discretionary spending pools to maintain discipline. Additionally, emergency fund planning should consider inflation, ensuring that the saved amount preserves its real value over time. These basic rules create a structure that is both flexible and resilient across uncertain economic climates.

Real-World Implementation Scenarios

Case Studies from Individual and Business Contexts

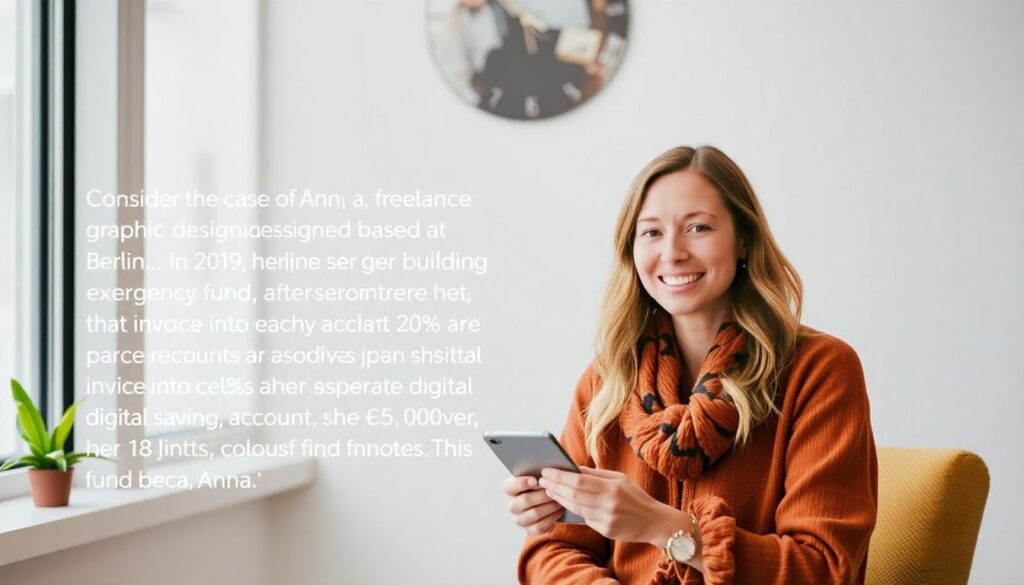

Consider the case of Anna, a freelance graphic designer based in Berlin. In 2019, she began building her emergency fund after experiencing inconsistent client payments. By setting aside 20% of each invoice into a separate digital savings account, she accumulated €9,000 over 18 months. This fund became essential when several projects were canceled during the early months of the COVID-19 pandemic. Her discipline in following targeted emergency fund strategies helped her avoid debt and maintain her rent and insurance payments.

Another example involves a mid-sized logistics company in Canada. The owner, aware of cyclical demand, implemented an emergency reserve equivalent to three months’ operational costs. When fuel prices spiked in 2022, the business used this cushion to absorb costs without downsizing. These real-world cases demonstrate that whether for personal or corporate finance, emergency fund tips rooted in foresight and regular contributions offer tangible protection against unpredictable disruptions.

Common Misconceptions and Pitfalls

Dispelling Myths That Undermine Savings Behavior

A widespread myth is that emergency funds are only necessary for low-income earners or financially unstable households. In reality, even high-income professionals can face sudden income loss due to layoffs or health emergencies. Another misconception is that credit cards or personal loans can substitute for emergency reserves. However, reliance on debt during crises often leads to a cycle of high-interest liabilities, exacerbating financial fragility.

Some individuals also believe that investing surplus cash is more efficient than saving it. While investments may offer higher returns, they come with market risk and potential liquidity issues—making them unsuitable for emergency fund planning. Lastly, many overestimate their ability to “cut back” in real time, failing to recognize the psychological and logistical challenges of rapid lifestyle adjustments. Addressing these misconceptions is crucial to foster realistic and sustainable emergency fund strategies.

Structured Approach to Building Your Fund

Five Actionable Steps for Financial Resilience

For those seeking a clear path on how to build an emergency fund, the following structured approach integrates best practices with modern financial tools:

1. Assess Monthly Essentials: Calculate your core expenses—housing, utilities, groceries, and insurance—to determine a realistic target (e.g., 3-6 months’ worth).

2. Automate Contributions: Set up automatic transfers to a high-yield, FDIC-insured savings account to ensure consistency.

3. Start Small, Scale Up: Begin with attainable milestones (e.g., $500, then $1,000), especially if you’re simultaneously managing debt repayments.

4. Separate and Protect: Keep the emergency fund in a dedicated account to avoid temptation and accidental withdrawals.

5. Review and Adjust: Reevaluate your fund biannually to account for life changes such as job shifts, inflation, or new dependents.

Implementing these steps offers a practical framework for emergency fund planning that adapts to both personal and macroeconomic uncertainties. The goal is not just to save, but to build a buffer that supports long-term financial stability.

Conclusion: Designing Resilience in the Face of Uncertainty

In an increasingly volatile global economy, a robust emergency fund is not merely a financial safeguard but a form of personal empowerment. The strategic application of emergency fund tips, rooted in historical lessons and real-life examples, reveals that preparedness is both attainable and essential. By dispelling myths and embracing structured planning, individuals and businesses alike can navigate uncertainty with greater confidence and control. The best ways to save for emergencies are those that align with individual circumstances while maintaining the flexibility to respond to the unknown.