Why your personal financial statements matter (and why they suddenly feel very 2025)

Before apps and robo‑advisors, people literally kept their finances in ledgers and envelopes. In the early 1900s, a “statement” might be a notebook with ink stains and a lot of guesswork.

Today, in 2025, you can connect your bank, broker, and even your crypto wallet to a dashboard in seconds. But the core idea hasn’t changed in over a century: write down what you own, what you owe, what you earn, and what you spend — then make decisions based on that picture.

That picture is your set of personal financial statements. Once you know how to compute and interpret them, every big money decision becomes less emotional and more informed.

We’ll walk through, step by step:

– What personal financial statements are

– How to create a personal financial statement from scratch

– How to read the numbers like a pro (even if you hate math)

– Typical mistakes beginners make and how to avoid them

No spreadsheets required — though they definitely help.

—

Step 1: Understand what “personal financial statements” actually are

For individuals, you really need just two core documents:

– Personal balance sheet – a snapshot of your financial position at a single point in time (today, for example).

– Personal income statement – a summary of your income and expenses over a period (usually a month or a year).

If you’ve ever seen personal balance sheet and income statement examples in a book or online, your own version will look similar, just in a simpler, more human way.

Think of it this way:

– The balance sheet answers: *“Where am I financially, right now?”*

– The income statement answers: *“What’s actually happening to my money over time?”*

Together, they make it a lot easier to see whether you’re moving toward financial stability or drifting away from it.

—

Step 2: Pick a simple personal financial statement template

You don’t need fancy software. A basic personal financial statement template can be:

– A simple Google Sheet or Excel file

– A notes app with headings and bullet points

– A printed worksheet you fill out by hand

At minimum, your template should have spots for:

– Assets (what you own)

– Liabilities (what you owe)

– Income (money coming in)

– Expenses (money going out)

If you later decide to use free personal finance tracking and budgeting tools, you can always copy the structure you’re about to build into whatever app you like.

—

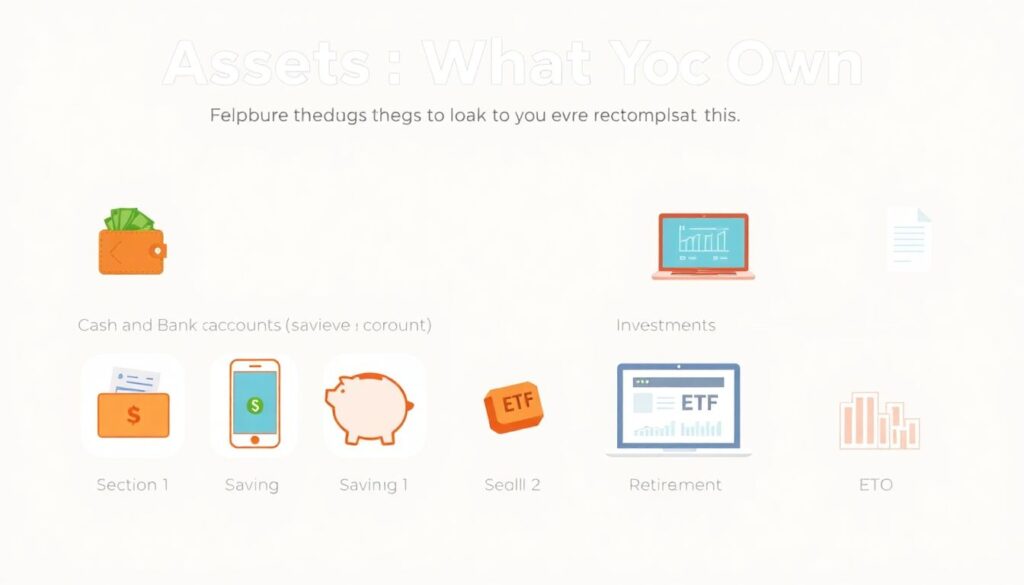

Step 3: List your assets (what you own)

Assets are things that have monetary value and belong to you. Don’t overcomplicate this. Start with big obvious items, then move to the smaller ones.

Common categories:

– Cash and bank accounts: checking, savings, digital wallets

– Investments: brokerage accounts, retirement accounts, ETFs, stocks, bonds, crypto (if you actually treat it as an investment)

– Property: your home, rental properties, land

– Vehicles: cars, motorcycles, boats, etc.

– Other: valuable collections, precious metals, significant business ownership

For each asset, write down:

– What it is (“Savings account at Bank X”)

– Its current value (current balance or fair market value)

Beginner tip:

When in doubt about the value (e.g., your car), use a realistic resale value from a reputable site rather than what you *paid* for it. Assets should reflect what you could roughly get if you sold them today.

Common errors to avoid:

– Counting stuff you’d never actually sell. Your couch and TV usually don’t belong here unless they are genuinely valuable and resalable.

– Using sentimental value instead of market value. Your guitar might be priceless to you, but your balance sheet cares about what someone else would pay.

—

Step 4: List your liabilities (what you owe)

Liabilities are your debts and obligations. This part is uncomfortable for many people, but it’s where the most useful insight often lives.

List every outstanding debt:

– Mortgage balances

– Student loans

– Credit card balances

– Personal loans / “Buy Now Pay Later” plans

– Car loans

– Tax debts or unpaid bills if they’re significant

Write down:

– Who you owe

– The total balance

– The interest rate (even roughly)

– The minimum monthly payment

Beginner tip:

Pull numbers from statements, not your memory. We almost always underestimate our debt when we “just remember.”

Mistakes to watch for:

– Ignoring small debts. Five “small” balances can easily add up to a big problem.

– Listing monthly payments as liabilities. The liability is the total amount you owe, not the monthly slice.

—

Step 5: Compute your personal net worth

Now you have:

– Total assets

– Total liabilities

Your net worth is simply:

> Net worth = Total assets – Total liabilities

That’s the core result of your personal balance sheet.

If it’s negative, don’t panic. Many people in their 20s and 30s have negative net worth due to student loans or early mortgages. What matters is the trend over time.

How to interpret your net worth:

– If your net worth is growing each year, even slowly, you’re generally moving in the right direction.

– If it’s flat or shrinking, something in your spending, saving, or investing pattern needs attention.

– Compare today vs. 12 months ago, not today vs. some ideal number you saw on social media.

—

Step 6: Build your personal income statement

Now you shift from “where I am” to “what’s happening every month.”

Choose a period — usually:

– The last full month

– Or the last 3 months if your income or expenses are irregular

Separate into:

– Income – salary, bonuses, freelance work, rental income, side gigs, dividends, interest, etc.

– Expenses – housing, food, transportation, debt payments, insurance, subscriptions, personal spending, etc.

If you use free personal finance tracking and budgeting tools, many will auto‑categorize this for you. If not, bank and card statements work fine — it just takes more manual sorting.

Key numbers to calculate:

1. Total income for the period

2. Total expenses for the period

3. Savings (or deficit) = Total income – Total expenses

If the result is positive, that’s your savings (even if you didn’t physically move it into a savings account). If it’s negative, that’s your shortfall.

—

Step 7: Interpret your income statement like a detective

Here’s where the numbers turn into insights.

Look for:

– Savings rate: What percentage of your income are you actually keeping? (Savings ÷ Income × 100)

– Fixed vs. variable expenses: How much is locked in (rent, insurance, minimum debt payments) vs. flexible (dining out, entertainment)?

– Debt drag: What portion of your income goes to interest and principal on debts?

A few rules of thumb (not laws, but useful signals):

– If your savings rate is under ~10%, your long‑term goals may be at risk without some changes.

– If debt payments take 30%+ of your income, that’s a red flag — you’re highly constrained.

– If most expenses are “fixed,” you’ll have less room to maneuver in a crisis.

Common misinterpretation:

People often say, “I don’t know where my money goes.” Your income statement should answer that clearly. If a category surprises you (“I spend *that* much on delivery food?”), that’s a signal, not a failure.

—

Step 8: Combine both statements into a real story

Now line up your personal balance sheet (net worth) and income statement (cash flow):

Ask yourself:

– Is my net worth growing by at least my annual savings?

If your investments lost money or debt interest ate your savings, net worth can stagnate even if you’re “saving.”

– Are my debts shrinking meaningfully over time?

For high‑interest debt, the balance should be dropping steadily, not just being maintained.

– Is my asset mix aligned with my goals?

Too much in cash might mean missed growth; too much in risky assets might mean sleepless nights.

This “story view” is what many personal financial planning and analysis services provide: they don’t just record your data, they interpret the trends. You can do a simpler version yourself once you know where to look.

—

Step 9: Avoid the classic beginner mistakes

As you build and analyze your statements, keep an eye out for these traps:

– Confusing income with wealth

A high salary with no savings and lots of debt doesn’t translate into a strong balance sheet. Your net worth tells the real story.

– Overvaluing illiquid assets

That stake in a startup or a friend’s business might be worth something one day — or nothing. Be conservative with anything that can’t be sold easily.

– Ignoring irregular expenses

Annual insurance premiums, vacations, or big repairs don’t show up every month, but they are real. Spread them out in your planning so they don’t feel like “surprises.”

– Never updating your numbers

A one‑time snapshot is helpful, but the real power comes from comparing this month vs. last year, or pre‑ and post‑major life events.

—

Step 10: Make your statements part of a simple routine

You don’t need a CFO mindset, but a light, regular process helps:

– Monthly (30–45 minutes):

– Update balances for major assets and debts

– Refresh your monthly income and expenses

– Note your savings rate and net cash flow

– Quarterly (about 1 hour):

– Compare net worth to last quarter

– Review any big category shifts in expenses

– Adjust goals or budgets if needed

– Annually (1–2 hours):

– Compare net worth to last year

– Check if you’re on track for big goals (home purchase, debt payoff, retirement savings milestones)

– Decide if you need outside help or more structure

Over time, this will feel less like “homework” and more like a dashboard for your life. You’re just checking the instruments, like a pilot.

—

Step 11: Using tools without losing understanding

It’s tempting in 2025 to outsource everything to apps and algorithms. Many platforms offer slick dashboards that look like corporate finance for your personal life.

Using free personal finance tracking and budgeting tools is totally fine, and often helpful. Just keep two principles in mind:

– You should still be able to recreate your numbers on paper.

If an app vanished tomorrow, you’d still know: what you own, what you owe, what you earn, what you spend.

– Treat categories and graphs as starting points, not final answers.

If an app says “You spent $600 on shopping,” drill down. Was that clothing? Home essentials? Gifts? The interpretation is what leads to better choices.

In other words, technology should speed up the computing, but you stay in charge of the interpreting.

—

Step 12: When DIY is enough — and when to get help

For many people, a simple homemade system, maybe based on a straightforward personal financial statement template, plus a couple of consistent habits, is plenty.

Consider seeking more structured personal financial planning and analysis services if:

– Your situation is complex (multiple properties, business income, large inheritance)

– You’re facing big one‑time decisions (retiring, selling a business, relocating countries)

– You’re overwhelmed emotionally by the numbers and keep avoiding them

A good professional will take your basic statements, refine them, and help you model future scenarios — but you’ll get far more value from that relationship if you already understand the basics you’ve just learned.

—

Final thoughts: your statements are a mirror, not a verdict

Your personal financial statements don’t judge you; they describe you. They show the result of past decisions and circumstances, not your future potential.

In 2025, with all the noise around “getting rich fast,” these simple, almost old‑fashioned tools — a balance sheet and an income statement — are still some of the most powerful ways to:

– See where you stand

– Understand what’s really going on with your money

– Decide what to change next

Compute them honestly. Interpret them calmly. Then use them to make one or two concrete improvements at a time. The numbers will start to shift, and over the next few years, your financial story will, too.