If you earn money online, you’re running a business, even if it feels like a side hustle. That means you’re playing in the world of taxes, financial regulations, and compliance—whether you like it or not. The good news: once you understand the basic rules, staying on the right side of the law is mostly about consistent habits and the right tools, not memorizing regulations.

—

Key terms you actually need to understand

Before going deeper, it helps to lock in a few core definitions. In the context of financial regulations for online businesses, compliance is simply the process of making sure your actions match what the law requires: reporting income correctly, paying taxes on time, and following anti‑money‑laundering and consumer protection rules where relevant. An online business is any structured activity that generates income via the internet: selling digital products, running an e‑commerce store, affiliate marketing, paid newsletters, SaaS, or streaming with donations and sponsorships. For regulators, a small Etsy shop and a big marketplace are just different sizes of the same thing: commercial activity subject to tax and reporting rules.

Another important term is tax residency. It’s not always the same as citizenship or the country printed in your passport. Tax residency usually depends on where you live most of the year and sometimes on where your “center of vital interests” is—family, home, main source of income. This matters because how to pay taxes on online income depends first of all on which country treats you as a tax resident, not where your clients or platforms are located. Finally, beneficial owner refers to the real person who ultimately receives the economic benefit from a business or bank account, even if that business is registered under a company or in another jurisdiction. Authorities increasingly care about the beneficial owner to fight tax evasion and money laundering.

—

How regulators “see” your online income

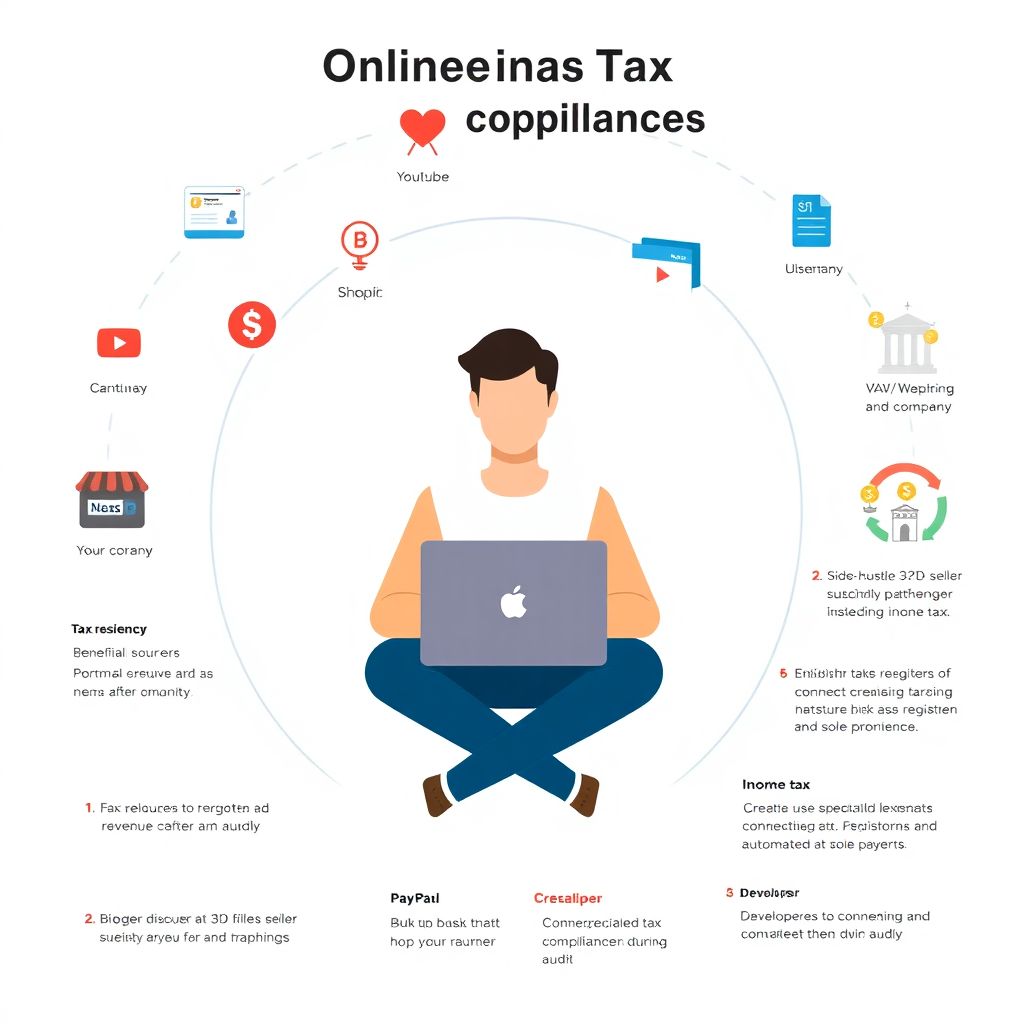

From your perspective, income might look messy: a bit of PayPal, some Stripe payouts, AdSense revenue, marketplace transfers, crypto payments from clients. From a tax authority’s perspective, this is all taxable income unless a specific exemption applies. It doesn’t matter that the money hits different platforms; what matters is that it’s the result of your economic activity. That’s why many online business legal compliance services start their work by mapping all your income streams into a single, structured ledger, even if you still think of them as “side gigs.”

Think of a simplified mental diagram:

[Diagram: “Income sources” (platforms like Upwork, Etsy, YouTube, Patreon, Shopify, crypto wallets) → “Payment processors” (PayPal, Stripe, bank accounts) → “You / Your company” → “Tax reporting and payments”.]

Regulators care primarily about the last arrow. They don’t mind that you use an intermediary platform; they care that the final recipient (you or your company) declares and pays taxes on the full amount before expenses, then deducts allowed costs according to local law. Many conflicts arise because creators only look at what arrives in their bank account and forget about fees withheld upstream by platforms or processors.

—

How to pay taxes on online income without losing your mind

At a practical level, how to pay taxes on online income breaks down into four repeating steps: track, classify, calculate, and file. Tracking means you keep a record of every payout and fee, including the gross amount before platform or payment fees. Classification means you label it correctly—business income, royalties, sponsorships, affiliate commissions, or interest. Calculation is where you apply your local tax rules: income tax, social contributions, possibly VAT/sales tax. Filing is the formal submission of your returns, plus paying the bill.

A lot of freelancers and creators still try to do this with spreadsheets, which quickly turns into chaos once you have more than one platform. That’s exactly where tax compliance software for freelancers and creators comes into play. These tools connect directly to your Stripe, PayPal, marketplaces, and sometimes even your crypto wallets. They consolidate transactions, tag them, and prepare tax‑ready summaries. Compared with manual tracking, the probability of missing a platform or misclassifying income drops dramatically, and the output is structured in a way most accountants and tax authorities recognize immediately.

—

Real case: the “forgotten” ad revenue channel

Anna runs a popular design blog and earns through sponsored posts and affiliate marketing. She diligently declared all affiliate payouts coming to her bank account but ignored the small, irregular income from an old AdSense account linked to a different email. She assumed, incorrectly, that “it’s so small it doesn’t matter.” After three years, the ad network started issuing annual income statements. Her tax office received matching information via international data exchange and noticed the missing income.

When she was audited, the inspector didn’t accuse her of fraud but recalculated her total income with late payment interest and a penalty for underreporting. The amount wasn’t huge, but the stress and time lost were. When she later onboarded with an online business legal compliance services provider, the first thing they did was an “income source discovery” checklist: they asked about every possible platform she’d ever connected to. The lesson: authorities increasingly get data from payment platforms directly; “small” income streams are still visible to them and must be declared.

—

Choosing a legal form and understanding your obligations

Another major compliance decision is whether you operate as an individual (sole proprietor, self‑employed) or through a registered company. Operating as an individual is usually simpler: fewer formalities, no corporate filings, and profits are taxed once as personal income. However, you often pay higher combined rates and have unlimited personal liability for business debts and consumer claims. A company (LLC, LTD, or equivalent) creates a separate legal person. Profits might be taxed at a corporate rate, then taxed again when distributed as dividends, but you often get better access to business banking, payment processors, and more predictable treatment in cross‑border operations.

Comparing the two is a good example of how legal structure impacts financial regulations for online businesses. With a company, you must keep corporate books, file annual reports in many jurisdictions, and sometimes appoint local directors or maintain a registered office. Non‑compliance can mean fines or even dissolution of the entity. With a simple freelancer setup, your obligations concentrate on personal income tax, social security contributions, and sometimes VAT registration if you cross thresholds. The optimal structure depends on your revenue level, risk profile, and where your main customers are located.

—

Case: from “hobby” to business overnight

Mark started selling 3D print files on a marketplace while working full‑time as an engineer. For two years, the income was a few hundred dollars per month, which he tagged mentally as “beer money” and never declared. Then one of his models went viral on social media, and revenue jumped to several thousand per month. The marketplace began requiring tax forms, and his bank asked questions about frequent foreign currency inflows.

Concerned, Mark booked paid legal advice for earning money online from a local tax attorney. They reviewed his past activity and concluded that, under his country’s law, he had been “running a business” from the first year, even if he didn’t register it properly. The lawyer helped him file voluntary corrections for previous tax years, which significantly reduced penalties compared to being audited first. More importantly, they registered him as a sole proprietor, clarified his deductible expenses (software, hardware, marketplace fees), and implemented a simple monthly reporting process. Within a year, Mark had a clean history and was able to apply for better credit, something that would have been risky if his accounts had been flagged for non‑compliance.

—

Handling cross‑border payments and platforms

Earning online often means income from multiple countries, but most legal obligations still anchor to your tax residency. The fact that your clients are in the US, your payment processor is in Ireland, and your platform is registered in Singapore doesn’t mean you can pick a jurisdiction arbitrarily. Typically, you pay income tax where you are a resident, unless you deliberately create a corporate structure in another country and manage it correctly from there (which has its own rules and risks).

One of the trickiest aspects is VAT / sales tax on digital products and services. Many countries tax the place of the customer, not the seller. Platforms like app stores and major marketplaces often collect and remit this tax on your behalf, but not always. You need to read their documentation carefully. In some situations, you may have to register either in a special “one‑stop shop” system or in multiple countries. Compared with local offline businesses, this adds complexity, but the principle is still the same: consumption is taxed where it happens. When choosing online business legal compliance services, verify they understand cross‑border indirect tax rules, not just income tax.

—

Diagram: money and responsibilities flow

Visualizing responsibilities can help avoid blind spots:

[Diagram: “Customer in Country A” → pays “Platform in Country B” → sends payout to “Creator in Country C”.

Above each arrow: “VAT / sales tax decision” at customer → “Platform terms & tax handling” at platform → “Income tax + reporting” at creator.]

In this chain, the customer mainly cares about paying the correct amount. The platform focuses on charging the right tax and issuing statements. You, as the creator, must ensure that whatever the platform does, you still declare the final income correctly and retain supporting documents (invoices, statements, contracts).

—

Using tools and services to stay compliant

Alone, it’s hard to keep up with every rule change. That’s why a practical strategy often mixes three layers: basic personal understanding, specialized software, and periodic professional advice. Your own understanding covers the “what” and “why”: you recognize which income is taxable, you know key deadlines, and you understand the difference between revenue and profit. Software handles the “how”: it reconciles transactions, calculates estimated tax liabilities, and stores structured records. Professionals—accountants and lawyers—handle edge cases, complex cross‑border setups, and communication with authorities if something goes wrong.

When evaluating tax compliance software for freelancers and creators, you want to check: does it integrate with your actual platforms (Etsy, Gumroad, Patreon, Twitch, Shopify, etc.)? Can it handle multi‑currency payouts and convert them using acceptable methods? Does it support your country’s reporting formats, or at least export data in a way your accountant can import? Compared with generic spreadsheets, specialist tools enforce consistency and reduce the risk of “forgotten” wallets or accounts. They also act as a form of documentation: if you are ever audited, having structured exports from a recognized system tends to build credibility.

—

Case: automation as audit protection

Sara is a content creator with income from memberships, ad revenue, and brand deals. At first, she logged everything manually in a spreadsheet. As her channel grew, she missed several invoices and forgot to include small foreign transfers from one brand that paid via Wise. Two years later, her country introduced stricter controls on international transfers. Her bank reported her incoming flows, which didn’t fully match her tax returns. The discrepancy triggered a “desk audit”—a request for clarifications and documentation.

Luckily, a few months earlier she had migrated to a specialized app that falls under the category of tax compliance software for freelancers and creators. The app had imported historical data from her platforms and bank accounts. With help from a local accountant, she used its reports to rebuild the missing pieces for previous years. Because she could show a coherent, time‑stamped dataset and evidence that she had tried to maintain order, the authority accepted amended returns with modest penalties. In her case, the software didn’t just save time; it practically saved her from a protracted investigation.

—

Step‑by‑step roadmap for staying compliant

To keep things concrete, here’s a practical sequence you can follow, whether you’re just starting or trying to clean up an existing online income stream:

1. Map all income sources

List every platform, marketplace, payment processor, bank account, and wallet that has ever received money connected to your work. Include even tiny or inactive accounts—authorities can still receive data from them. This initial inventory reduces the risk of “orphaned” income that never gets declared, which is a common trigger for tax questions and retroactive assessments.

2. Determine your tax residency and applicable regimes

Verify officially where you are considered a tax resident. Check if there are special regimes for small entrepreneurs, digital nomads, or creators in your jurisdiction. Many countries offer simplified schemes with flat rates or simplified bookkeeping if your revenue is below a threshold. Understanding which regime applies is more important than chasing rumors about “tax‑free” countries on social media.

3. Choose your operating form (individual vs. company)

Based on your revenue projections and risk tolerance, decide whether to stay as an individual or register a company. Here is where legal advice for earning money online is especially valuable: a local specialist can tell you how banks, platforms, and tax authorities treat each option in practice, not just in theory. For many, starting as an individual and converting to a company once consistent income is reached is the most efficient path.

4. Implement bookkeeping and record‑keeping tools

Set up accounting or tracking software that can consolidate data from your main platforms. Configure automatic imports where possible and schedule a monthly “finance hour” to reconcile balances. Keep copies of invoices, contracts, royalty statements, and payout reports. Even a simple, consistent system beats an elaborate one you never maintain.

5. Create a tax calendar and funding habit

Mark all relevant tax deadlines—quarterly prepayments, annual returns, VAT filings—into your calendar with reminders. Each time you get a payout, move a fixed percentage into a separate “tax buffer” account. This transforms tax payments from a crisis event into a predictable expense. Many experienced online entrepreneurs treat this buffer as non‑negotiable, similar to rent or payroll.

—

Risk zones and how to avoid them

Certain behaviors repeatedly show up in enforcement cases. One classic pattern is “platform hopping”: opening new accounts on different services each time an old one gets restricted or when terms change, without central tracking. On their own, multiple accounts aren’t illegal, but they dramatically increase the chance that some income will be left out of your books. Another risk is ignoring local regulatory triggers such as revenue thresholds that require VAT registration or cross‑border payment reporting in your country. These thresholds often change, and platforms aren’t responsible for notifying you.

A subtler issue is receiving payments in crypto without solid documentation. Many jurisdictions now treat crypto received for work as ordinary income at the fair market value at the time of receipt. If you only keep the wallet history but no contract or invoice, it can be harder to prove the nature of the transaction. In practice, the safest approach is to treat crypto just like any other payment method in your records: invoice, description of work, date, value in your reporting currency, and proof of receipt.

—

Case: crypto payments and missing paperwork

Leo is a developer who accepted partial payment in cryptocurrency from foreign clients to avoid high transfer fees. For a while, this seemed practical: instant settlement, no bank friction. He did not, however, adjust his invoicing routine. Instead of issuing formal invoices, he relied on chat logs and wallet addresses. A few years later, his country tightened rules around crypto and started asking detailed questions about large wallet balances.

When contacted by the tax authority, Leo had to reconstruct the economic history behind hundreds of transactions. Because he hadn’t documented the business purpose clearly, some incoming transfers were initially treated as “unexplained gains,” which in his jurisdiction could be taxed harshly. After hiring a specialist in financial regulations for online businesses, he implemented proper invoices and long‑term record‑keeping. The adviser also helped reclassify several transfers as legitimate business revenue, calculated at historical exchange rates. The process was painful but avoidable: the same simple discipline he used for fiat payments should have applied to crypto from day one.

—

When you should definitely talk to a professional

There are situations where DIY research is not enough, even with good software. If you are planning to move countries while keeping your online business running, open or close a company in a foreign jurisdiction, or if you receive a formal letter from a tax authority that you don’t fully understand, it’s prudent to seek specialized help. Professional online business legal compliance services and local tax advisers can interpret not only the written law but also administrative practice—how rules are enforced in reality.

Compared with guessing via forum posts, a short, targeted consultation can save years of compounding mistakes. It’s mostly about risk management: at low income levels with simple structures, your risk of major penalties is limited, but as revenue grows and your structure becomes more complex, regulators expect more from you. Aligning your tools, behavior, and advice with that expectation is the practical way to stay compliant while still benefiting from the flexibility of earning online.

—

Staying compliant with financial laws when earning online is less about fear and more about building robust, repeatable habits: knowing how your jurisdiction works, keeping complete records across platforms, using technology intelligently, and calling in experts when decisions become structural rather than tactical. With that foundation, your focus can return to growing the business, not worrying about the next letter from the tax office.