Setting financial boundaries sounds stiff and old‑school, but in 2025 it’s actually one of the few money skills that scales with the way we really live now: subscriptions everywhere, instant credit, buy‑now‑pay‑later hooks, income from side gigs and platforms instead of one stable salary. Boundaries are less about “don’t buy lattes” and more about creating a set of clear digital and psychological guardrails, so your money follows your priorities instead of your impulses or the algorithms that want you to spend just a bit more every day.

—

What “financial boundaries” actually mean in 2025

Фinancial boundaries are not just limits; they’re rules about *access* to your money, your time and your attention. In technical terms, a financial boundary is a pre‑defined constraint on how, when and with whom financial resources can be used. That includes: who you share accounts with, how much you allow yourself to spend in specific categories, what you’re willing to lend to friends, and even how often you check trading apps. Unlike a simple “budget”, which is usually a static monthly plan, boundaries are dynamic and behavior‑oriented: they aim to block or redirect actions *before* money leaves your account. This difference is crucial in a world where a five‑second tap can turn a random ad into a recurring charge you’ll forget about in two weeks.

—

Key terms you need before you start

Spending limit vs. financial boundary

A spending limit is numeric: “I spend no more than $300 on restaurants this month.” It’s a parameter, usually inside an app or spreadsheet. A financial boundary is broader: “If I’ve hit my restaurant cap, I switch to cooking at home, and I do *not* override the cap unless there’s a genuine emergency.” The limit is the number; the boundary is the rule plus the enforcement. In practice, boundaries often live across multiple tools: your bank app, your personal finance planner to set spending limits, and your internal agreement with yourself. That multilayer structure matters, especially now that different apps try to upsell you constantly with “one‑time boosts” and quick increases in credit lines.

Hard vs. soft boundaries

A hard boundary is binary: “No borrowing money to friends,” “No new credit cards this year,” or “Rent may never exceed 35% of net income.” Soft boundaries allow some controlled flexibility: “I prefer to spend $200 on clothing, but in months with a work event I may push it to $250 as long as I lower entertainment.” In 2025 the most sustainable setups combine both: the hard boundaries protect you from catastrophic drift (long‑term debt, housing overreach), while soft boundaries give room for real life to happen without guilt. This layered design replaces the older, rigid envelope system that often collapsed as soon as real life deviated from the plan.

—

Why boundaries beat traditional budgeting

Classic budgeting treated money like a static spreadsheet: one income source, predictable expenses, and a single “monthly plan” that you tried (and often failed) to obey. Today we face variable incomes, micro‑transactions, and attention‑hacking interfaces. Boundaries work better because they integrate behavior design and friction into your money system. Instead of only tracking where money went, they change how easy it is for money to go there in the first place. Compared to old‑school budgets, boundaries pair excellently with real‑time controls: card‑level limits, merchant locks, or auto‑transfers that move money out of your “spendable” account right after payday. This makes your willpower less central and the system more reliable when you are tired, stressed, or doom‑scrolling at 1 a.m.

—

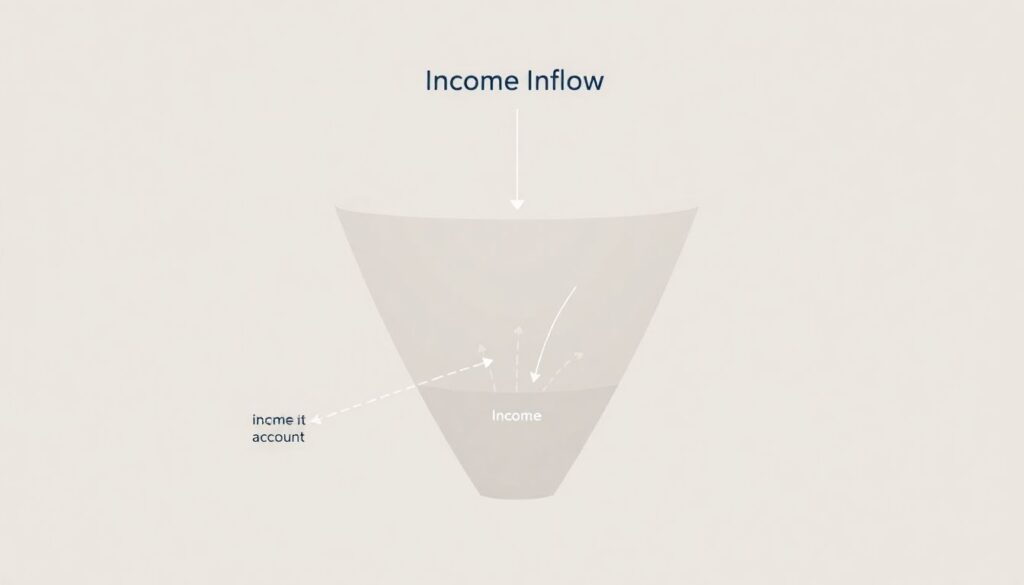

Diagram: how boundaries fit into your money system

Visualize your budgeting routine as a simple vertical diagram:

1. Top layer – Income inflow

Think of this as arrows coming from salary, gig work, freelance platforms and passive income into one main “hub” account. This is the widest point of the diagram, like a funnel mouth, collecting all inflows regardless of source or timing.

2. Middle layer – Boundary filters

Below that hub, imagine a set of horizontal filters, each labeled with a boundary: “Essentials”, “Goals”, “Fun”, “No‑go”. Money flows through these filters according to pre‑set percentages or rules. The “No‑go” filter routes money away from categories you have explicitly blocked, such as high‑risk trading or impulsive shopping apps.

3. Bottom layer – Concrete actions

The filtered streams feed your actual accounts and cards: bills account, savings vaults, investment accounts, and your day‑to‑day spending card. Each account is relatively narrow in the diagram, representing limited access and defined purpose, which is the technical expression of your boundaries.

This verbal diagram highlights a modern twist: boundaries work as filters between income and behavior, not as a static report after the fact. The more of these filters you automate, the less you’ll rely on memory or discipline to keep your budgeting routine healthy.

—

Modern trends shaping financial boundaries in 2025

In 2025, three trends are reshaping how people think about healthy money boundaries. First, financial apps have adopted behavioral design, adding “cool‑down” timers, contextual warnings, and category‑based locks that serve as software‑level boundaries. Second, social money culture has shifted: instead of flexing luxury purchases, more creators are sharing “no‑spend weekends” and transparent debt paydown journeys, which normalizes saying no. Third, hybrid learning formats have exploded; for instance, an online workshop on healthy money boundaries can include live coaching, AI‑driven spending analysis and interactive simulations, letting you test boundary scenarios before applying them to real money. These innovations make it easier to build guardrails that fit your lifestyle and emotional triggers instead of blindly copying generic budget templates.

—

Step‑by‑step: how to design your own financial boundaries

1. Audit where your boundaries are already weak

Start by mapping the spots where your money behavior regularly contradicts your intentions. Look for patterns rather than isolated incidents: late‑night shopping, random trading after watching hype videos, “small” subscriptions that never end, or lending money you can’t really spare. Use your banking dashboard or a tracking app and scan the last three months. Notice not just categories but also *contexts*: time of day, who you were with, which app you used. This context is the raw data you need to design precise boundaries that aim at the actual trigger, not the abstract category. You are building a diagnostic profile of your budget’s weak points, a bit like a risk map in cybersecurity.

2. Translate pain points into explicit rules

Next, convert those weak spots into boundary statements. These should be measurable, time‑bound, and ideally enforceable with tech. Instead of “I’ll try to eat out less,” define: “Restaurant spending capped at $220 per month, card gets frozen for restaurant MCC codes once the cap is hit.” Or “No investments made within 24 hours of discovering them; I bookmark options and revisit the next day.” Each rule needs a trigger (“when X happens”), a limit (“up to Y”), and a consequence (“then Z occurs automatically or I must do A instead”). This is where a financial boundary setting course can help: many of them walk you through converting vague goals into concrete, operable constraints that can be encoded directly into your banking tools.

3. Build a boundary‑aware budgeting routine

Now embed those rules into a recurring routine. Once a week or twice a month, you should run a short “boundary check” instead of a generic budget review. Ask: which boundaries held, which got overridden, and why? This is less about judging yourself and more about debugging a system. Maybe you set your clothing cap too low given your work dress code, so you’re constantly tempted to break it. Modern budgeting apps can now send you nudge reports (“you are 85% towards your restaurant limit by mid‑month”), which you can treat as early‑warning signals. Over time, this routine forms the backbone of a healthier budgeting rhythm where your focus is on behavior rules, not just numbers on a dashboard.

—

The role of tools: planners, apps and automation

Using planners and apps as guardrails, not just trackers

The old way to use a budget app was to log expenses and look at charts at month’s end. In a boundary‑first approach, your software becomes an active gatekeeper. A modern personal finance planner to set spending limits will let you define per‑category caps, auto‑transfer rules, and alerts that escalate from gentle reminders to hard blocks. The tech term for this is “pre‑commitment mechanisms”: you change what future‑you is allowed to do with money. In 2025, better apps also visualize opportunity costs in real time: when you raise your vacation budget, you instantly see how that delays your debt payoff date, which makes boundary trade‑offs more tangible and less abstract.

How automation enforces boundaries in the background

Automations are where your boundaries become almost self‑enforcing. You can set your main account to sweep a fixed percentage of every income inflow into a separate “untouchable” savings vault. You can connect subscriptions to a dedicated card that has a low limit and gets manually topped up monthly; if there’s not enough balance, the subscription fails instead of quietly hitting your core account. Some neo‑banks in 2025 even support merchant‑level locks, so you can literally blacklist specific online stores and unblock them only after a deliberate review. This is a step beyond legacy budgeting: you are adding friction to the exact places where you tend to overspend, making spontaneous boundary violations inconvenient by design.

—

Human support: when and how to get professional help

Even with great tools, money behavior is emotional and social. If you find yourself repeatedly overriding your own rules, or if money conflicts with partners or relatives keep recurring, consider outside support. A budgeting coach for setting financial boundaries can help you identify the beliefs and emotional triggers behind your patterns, then co‑design rules that you actually respect under stress. If you prefer structured learning, joining a live or asynchronous financial boundary setting course gives you a blend of education, templates, and peer support, which often speeds up implementation. Don’t underestimate how much easier it is to say “I have a rule” when that rule was built in a formal process with someone you consider an expert.

Sometimes the issue is less knowledge and more accountability or complexity. In that case, looking for professional help to improve budgeting habits makes sense, especially if you’re juggling business expenses, shared family finances, or multiple income sources. A professional can audit your system, suggest specific automations, and point out legal or tax angles you might miss. The emerging norm in 2025 is to treat financial health like mental or physical health: totally normal to get specialized help instead of trying to brute‑force everything alone with yet another spreadsheet.

—

Boundaries in relationships and shared finances

Boundary work becomes more complex when your money intersects with other people. Co‑habiting, co‑founding a startup, or supporting relatives all create overlapping claims on your income. Instead of vague understandings, define explicit agreements: which expenses are shared, what the maximum shared budget is, and where each person keeps their independent funds. Technically, this often means maintaining at least three buckets: “mine, yours, ours.” A clear rule might be: “Joint account covers rent, utilities and groceries up to X; all other spending is from personal accounts, no questions asked unless it affects our joint savings goal.” These lines reduce conflict because you no longer negotiate every decision; you just apply agreed boundaries.

A modern twist in 2025 is the spread of collaborative money tools where partners can see joint goals and boundary dashboards without fully merging accounts. You can, for example, share visibility into a vacation fund but keep individual spending private. This avoids the extremes of full secrecy or total financial fusion. If money conversations feel loaded or you come from very different backgrounds, a short series of sessions with a coach who focuses on couples and boundaries can be more productive than endless arguments about single purchases.

—

Comparison: boundaries vs. other popular approaches

To understand why boundary‑based budgeting is gaining traction, it helps to compare it with a few common analogs. Simple expense tracking is purely descriptive: it tells you what happened but doesn’t change the underlying behavior. Traditional zero‑based budgeting tries to pre‑assign every dollar but often fails when real life deviates from the plan, leading people to abandon the system. Pure frugality focuses on spending as little as possible, which can create a scarcity mindset and rebound splurges when willpower runs out. Minimalism aims to reduce possessions and commitments, but without clear numeric rules you can easily over‑spend on “high‑quality essentials”.

The boundary model borrows the best of each, but adds enforcement and realistic flexibility. From tracking, it takes data; from zero‑based budgeting, intention; from frugality, prudence; from minimalism, focus. But unlike those analogs, a boundary system doesn’t require you to perfectly predict your month or suppress all desires. Instead, it builds specific, testable rules plus automated guardrails. That’s why it scales better with gig‑based incomes, fluctuating costs, and the constant stream of new digital temptations that characterize 2025.

—

Practical examples of healthy financial boundaries

To anchor all this in reality, consider a few boundary setups that people are using right now:

1. Subscription firewall

All recurring payments run through a dedicated “subscriptions” card with a hard $80 limit. New subscriptions can only be added during a scheduled monthly review; impulse sign‑ups in the middle of the night are blocked by default.

2. Social spending cap

Dining out and drinks have a shared monthly limit, visible to both partners in a shared app. Once the total reaches the ceiling, any additional socializing switches to free or cheap options: home dinners, walks, or coffee at home. No exceptions unless both explicitly agree which other category will be reduced.

3. Impulse delay rule

Any non‑essential purchase above a chosen threshold (say $100) must sit in a “waiting list” for 72 hours. The shopping cart is saved, and a reminder pops up later asking if the item still fits current priorities. Many people discover that a surprising share of “must‑have” buys lose their appeal over a few days.

4. Gig income split

All side‑hustle income is automatically split: 40% to taxes and obligations, 40% to long‑term goals, 20% to guilt‑free fun. This prevents lifestyle creep while keeping motivation high, because each gig immediately feeds a visible progress bar for a goal that actually matters.

Each example shows the same pattern: concrete trigger, clear limit, and a default behavior once that limit is reached. That structure is what makes the boundary durable when your mood, energy or social pressure fluctuate.

—

Using education to upgrade your boundaries

If you want to accelerate the process, structured learning environments can compress years of trial and error into weeks. A good financial boundary setting course will typically cover behavior design basics, app configuration, scripts for difficult money conversations, and common failure modes (like letting “special occasions” blow up half your yearly progress). In 2025, many of these courses embed AI‑based simulations: you can test how your system reacts to a sudden income drop, a windfall, or a large unexpected bill, and refine your rules before real life throws these events at you.

Similarly, an online workshop on healthy money boundaries can give you live feedback on your draft rules, plus examples from people in similar life stages—freelancers, solo parents, digital nomads, or early‑career professionals. Combining that with a solid personal finance planner to set spending limits and smart banking tools gives you an ecosystem where your boundaries are documented, visible and mostly automated. The goal is not perfection, but a system that is robust enough that occasional slip‑ups don’t derail your whole budgeting routine.

—

Bringing it all together

Setting financial boundaries for a healthier budgeting routine in 2025 is less about austerity and more about architecture. You’re not just cutting costs; you’re designing a structure that channels your income toward what you actually value, while softening the impact of stress, fatigue and digital temptation. Clear terminology, well‑defined rules, smart use of tech, and, when needed, professional help to improve budgeting habits all work together to create that structure.

The most important shift is mental: stop treating money management as a monthly guilt session and start treating it as an ongoing design problem. You test a boundary, watch how it behaves under real conditions, then iterate. When you do that consistently, your budget stops feeling like a fragile promise and starts feeling like infrastructure—quiet, sturdy, and finally working for you instead of against you.