Balancing Ambition and Reality: Living on a Budget While Chasing Big Financial Dreams

Ambitious financial goals — like buying a home, retiring early, or launching a business — often seem incompatible with a tight personal budget. But the truth is, some of the most financially successful people started with modest means. The key isn’t about how much you earn, but how well you manage what you have. This article explores how to live within your budget while keeping your eyes on big financial outcomes — and how to avoid common first-timer pitfalls.

Understand Your Financial Baseline

Before striving toward big goals, you must know where you currently stand. A surprising number of people underestimate their monthly expenses or assume inaccurate income projections. In real practice, this leads to missed savings targets or accumulating unintended debt.

Start by calculating your average monthly income and tracking every expense for at least 30 days. Use budgeting apps like YNAB (You Need a Budget) or even a simple Google Sheet. Include everything — rent, groceries, subscriptions, healthcare, transportation, and even the occasional latte. This exercise is often eye-opening.

Real-World Insight

Take Anna, a junior designer in New York earning $52,000 annually. She aimed to save for a $20,000 down payment on a condo in five years. When she tracked her spending, she found $450 a month going to takeout and rideshares — nearly $5,400 yearly. By cooking more and biking to work, she redirected those funds into her savings, reaching her goal ahead of schedule.

Set SMART Financial Goals

Vague aspirations like “get rich” or “save more money” rarely lead to action. SMART goals (Specific, Measurable, Achievable, Relevant, and Time-bound) force clarity and commitment.

For example:

– Vague: “I want to save money.”

– SMART: “I will save $10,000 in 24 months by setting aside $417 per month.”

Break goals into smaller benchmarks and automate your savings where possible. This not only strengthens discipline but also integrates your goals into your everyday routine.

Technical Detail: Budget Allocation Frameworks

One popular method is the 50/30/20 rule:

– 50% of income to needs (rent, utilities, groceries)

– 30% to wants (entertainment, travel)

– 20% to savings and debt repayment

If you’re aggressively saving, consider a more extreme tilt — like 60/10/30 — where you live frugally and channel more toward saving.

Common Mistakes New Budgeters Make

Newcomers to budgeting often sabotage their progress unintentionally. Here are the top pitfalls to avoid:

- Underestimating Irregular Expenses: Annual car registration, holiday gifts, or medical co-pays don’t occur monthly but still affect your budget. Create a “sinking fund” — a savings bucket for periodic expenses.

- Failing to Adjust for Lifestyle Inflation: When income rises, many also increase spending. Stay disciplined and direct raises to investments or savings instead of luxury upgrades.

- Not Tracking Small Leaks: A $4 coffee every weekday is nearly $1,000 a year. Small habits compound quickly — positively or negatively.

- Over-restricting the Budget: Extreme austerity is unsustainable. Allow modest flexibility for entertainment and joy, or risk budget burnout.

- Skipping Emergency Funds: Without a buffer, any unexpected cost (even $500) can wipe months of savings or push you into debt. Aim for at least 3 months’ worth of essential expenses.

Maximize Your Income Potential

Living on a budget doesn’t mean you’re stuck with your current income. Explore side hustles, freelance gigs, or upskilling for higher-paying roles. Platforms like Upwork, Fiverr, and Skillshare offer monetization and learning opportunities. A second income stream can accelerate your progress toward big goals.

Example from Practice

David, a school teacher earning $38,000 annually, started tutoring online evenings twice a week. He brought in an extra $400/month, which he used exclusively to pay off his $12,000 student loan in just over two years — cutting his expected payoff time in half and saving hundreds in interest.

Invest Early, Even in Small Amounts

Many people delay investing because they think they need thousands to start. But with platforms like Fidelity, Vanguard, or even apps like Acorns and Robinhood, you can begin with as little as $50. Thanks to compound interest, starting early often matters more than investing a large sum later.

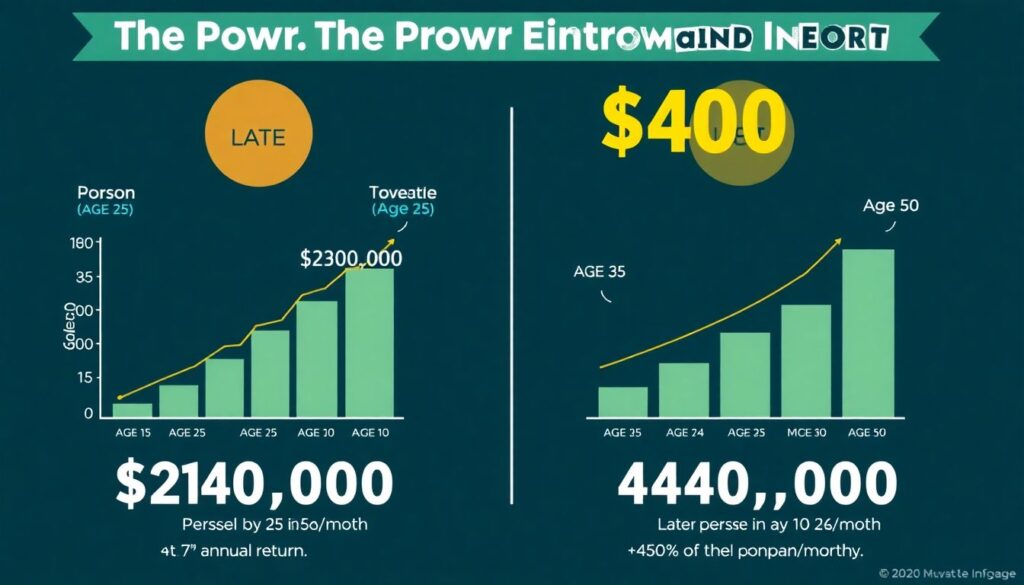

Quantitative Insight

If you invest $200/month from age 25, assuming a 7% annual return, you’ll have about $240,000 by age 50. Wait 10 years, and you’ll need $400/month to hit the same target — that’s the power of compounding working for (or against) you.

Final Thoughts: Discipline and Patience Beat Luck

Living on a budget while pursuing major financial goals isn’t glamorous — but it’s immensely empowering. You learn to take charge of your resources, prioritize what truly matters, and build a foundation for lasting wealth. Remember: it’s not about deprivation, but intentional living.

Reframe budgeting from a limitation to a launchpad. With consistency, even modest incomes can fuel extraordinary futures.